Time To Take Some Insurance

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

Equity investors have been glass half-full since July:

· Pricing out tariff, inflation, geopolitics

· Pricing in financial condition easing, RINO (recession in name only), and belief in AI RoI

The result:

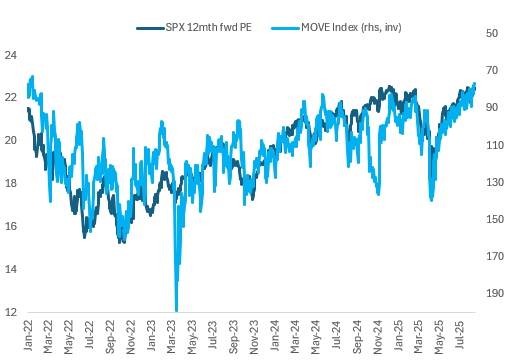

· Valuation multiples at multi-year highs: Expansion to ~22.5x 12m fwd earnings

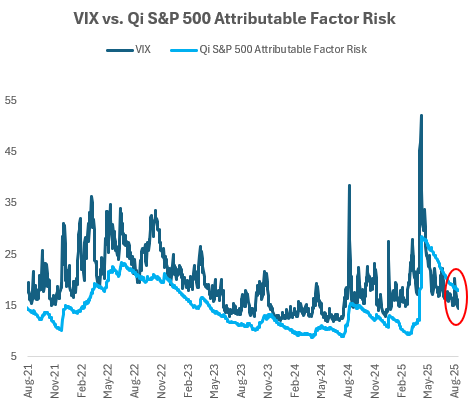

· VIX at YTD lows with a 14-15 handle

BUT Quant Insight’s model forecast for S&P500 annualised vol on macro alone is 18.

3 observations:

1. It is rare for Qi’s factor vol forecast alone to be higher than implied vol. See Chart 1

2. The market is implying that idiosyncratic drivers detract from spot risk.

3. Macro dominates Qi’s risk forecast BUT the decline in rate vol & credit spreads has been supporting valuations. See Chart 2

Arguably into late summer, the growth / inflation trade-off starts to be bite:

· ISM Services Prices Paid = 70

· Core PPI saw the biggest MoM jump since 2022

· Labour demand is cooling

· Inventories can’t cushion margins forever

Given the above, and as we head into the seasonal weakness of September, worth thinking about some insurance?