Stop Alpha Leakage

Isolate true alpha. Manage regime risk. Turn macro into edge.

Our Partners

.png)

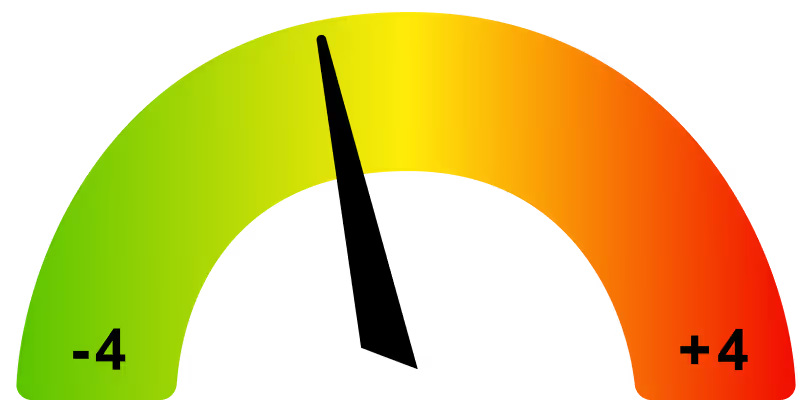

Macro Risk Pulse

The MRP is calculated using Quant Insights’ proprietary Macro Factor Equity Risk Model (MFERM)

-1.70

The Macro Risk Pulse (MRP) measures the proportion of total S&P500 risk explained by macro factors.

A high reading indicates that the market is predominantly driven by top-down macro factors opposed to company fundamental factors.

(The published figure is from the previous day closing data)

Who we help

Built for portfolio managers, CROs, and risk teams at institutional funds. Whether you run long/short equity or multi-asset strategies, MFERM gives you the macro layer that traditional models miss.

Equity Portfolio Teams

See what's really driving your returns. Construct stronger portfolios. No guesswork.

Multi Asset Teams

Know the fair value of 18,000+ securities. Across every asset class. Updated daily.

Trusted by funds who trust nothing.

Our Solutions

MFERM reveals how macro forces drive your portfolio—daily. See your true exposures. Track regime shifts in real-time. Separate macro from alpha. Turn macro into a source of edge, not just risk control. Built by former macro PMs who know what matters.