1. Equity winners & losers from EURUSD upside

2. Lower quality corners of the market stretched

3. EURUSD- multi factor macro!

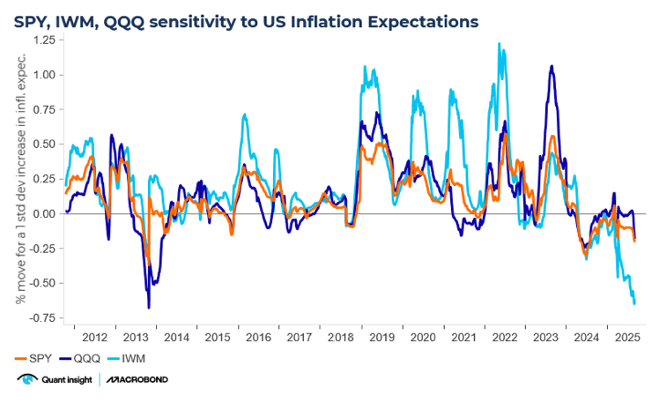

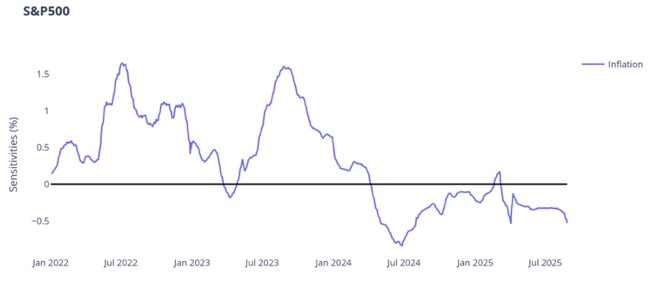

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

1. Equity winners & losers from EURUSD upside

As the rally in EURUSD continues, equity investors are increasingly focusing onthe relative winners & losers from a stronger Euro / weaker Dollar. The next earnings season will provide bottom-up anecdotal clues but, in the meantime, Goldman's basket of European companies with high sales exposure to the US now sits 1.5 sigma (5.6%) cheap to aggregate macro conditions.

The biggest driver of Qi's model is the desire for a weaker Euro, so this EURUSD rally has been abig drag on macro-warranted model value. But the basket also wants tighter credit spreads & low interest rate volatility. And the market has delivered on both which has provided a counterweight. Hence Qi model value has moved sideways.

In short, even with the Euro's recent strength, the basket has overshot to the downside.

2. Lower quality corners of the market stretched

Under the hood of this rally, we see stretched Qi Fair Value Gaps within the lower quality / more speculative areas of the market.

1. GS Very Important Shorts – FVG at upper end of multi-year range. Is the forced buying close to drying up? See the firstv chart

2. ARKK – FVG at upper end of multi-year range and starting to close. ARKK has rallied >70% from its April lows. See the second chart

3. GS Strong vs. Weak Balance Sheet L/S – FVG at bottom-end of multi-year range. In other words given the rally in HY, how much risk premia is there left to exploit? See the third chart.

Along with PB data highlighting HF gross exposure is high, this suggests there will be greater selectivity into this Q2 earnings season.

3. EURUSD – multi factor macro!

The bond market narrative is shifting. For months, inflation & deficit fears drove the steepener trade. Now a potential dovish Fed shift, SLR reform & supply changes (tilting issuance from bonds to bills) are starting to steal the headlines. Markets are considering the potential for lower long-term yields & flatter yield curves.

These changes are critical for FX investors too. Qi's EURUSD retains strong explanatory power (RSq has been high & stable throughout 2025) but the drivers have evolved - the bond market's impact has become more nuanced.

Interest rate differentials still matter but EURUSD is also showing growing sensitivity to:

· inflation differentials - relative European (US) reflation helps EURUSD upside (downside)

· curve shape - a flatter EUR (US) yield curve helps EURUSD upside (downside)

· EuroZone Sovereign Confidence - tighter (wider) peripheral spreads help EURUSD upside (downside)

That's a lot for FX investors to track but the good news is Qi's model orthogonalizes all these relationships & puts aggregate macro-warranted model value at 1.1725 currently.

.png)