1. A turning point in the everything rally?

2. If Trade Wars Are Over, Is the CAC Too Cheap?

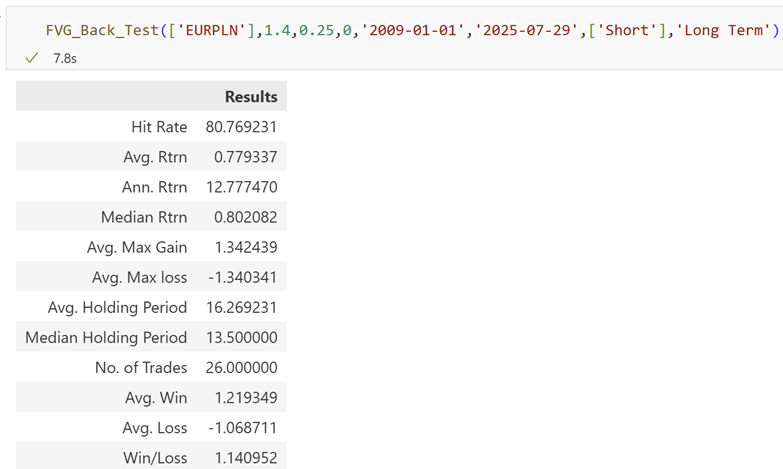

3. EURPLN - Another Chance for Poland Bulls

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

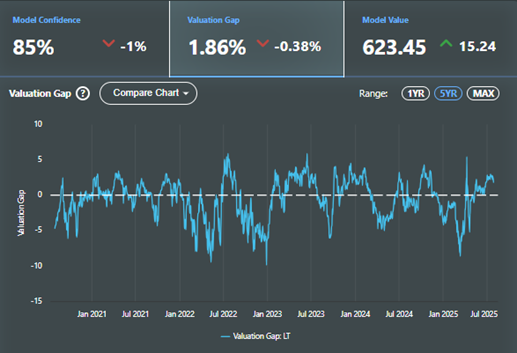

1. A turning point in the everything rally?

SPY spot is currently +0.5 sigma (~2%) above Qi model value – at the upper-end of its historical fair value gap range (see below). Indeed, 10 of the major 11 GICs sectors trade above Qi model value.

Further, a number of rich to model valuation gaps have opened up in lower quality / more speculative parts of the market.

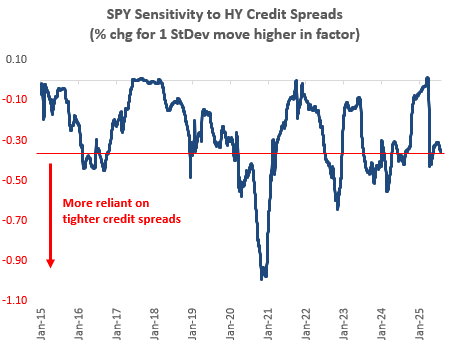

The reliance on the tighter HY credit spread propeller is large. The negative Qi sensitivity of SPY to wider HY credit spreads is heading towards multi-yearhighs:

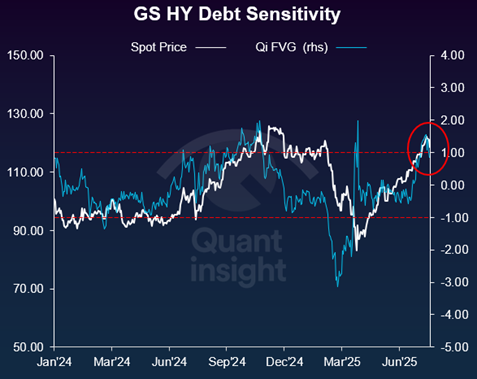

We highlight below a basket of high yield debt companies (GSXUDEBT) which is trading 0.85 sigma (~7%) above Qi model fair value – close to multi-year highs. The Qi FVG of this basket tracks the spot price well i.e. we should pay heed to the mean reversion potential after a 43% rally from the April lows.

2. If Trade Wars Are Over, Is the CAC Too Cheap?

An optimistic view would suggest the US-EU trade deal removes policy uncertainty and therefore abig tail risk for risky assets. In which case, the hunt is on for cheap laggards.

European equity indices have enjoyed a strong start to 2025. The pan-European Euro Stoxx 50 is up around 10%; German, Italian and Spanish indices are all up around 20%. The CAC is the outlier up just ~6.5%.

On Qi, the CAC 40 screens as 0.9 sigma (3.45%) cheap to model fair value. Aggregate macro conditions continue to improve, but the CAC's progress has stalled.

Model confidence is below our 65% threshold for a macro regime and therefore adds a health warning. Still, for those who believe the trade agreement was the least worst deal and markets can move on from trade wars, the CAC looks interesting.

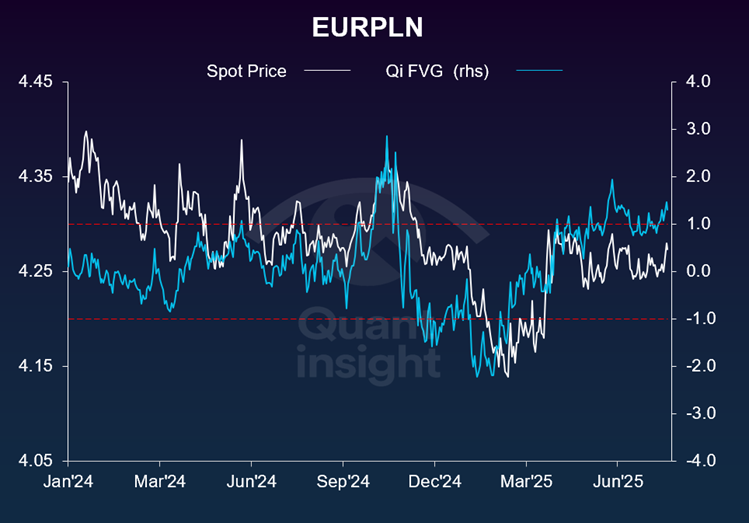

3. EURPLN- Another Chance for Poland Bulls

Poland has been a star performer in 2025 - the WIG has risen 36%. Some profit-taking is inevitable and disappointment around the US-EU trade may be the catalyst for that.

But, in FX, the move in EURPLN is starting to move into extended territory - the cross sits 1.4 sigma (1.6%) rich to Qi model value. Again, there's an amber flag from low model confidence. However, it is worth noting decent correlation between spot EURPLN and Qi's FVG suggesting mean reversion has recently tended to occur via the market re-pricing to macro.

Furthermore, even when relaxing our model confidence constraint, back-tests suggest these are historically significant levels.

.png)