1. Credit protection in equities undervalued

2. Small caps - too far, too fast?

3. CHFJPY- cross asset red flag, or FX idiosyncrasy?

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

1. Credit protection in equitiesundervalued

Tariff announcements seem to have lost their shock value for equity markets. Is this a sign of complacency? Credit protection as expressed in equities through the GS Strong vs. Weak balance sheet basket pair looks undervalued. Qi’s Fair Value Gap forthis basket RV stands at -1.74 sigma, close to multi-year lows.

It is a rare even treaching this level only 6 times since 2009 but 5 out of those 6 times the basket delivered positive returns over the next month. See the back test simulative results below.

The FVG of this pair has a good correlation tothe spot price – should this basket start to make gains it would be synonymous with market nervousness edging higher.

2. Small Caps – too far, too fast?

There is increased investor interest in rotation trades into the laggards & small caps are often cited as the major beneficiary of such a move. Qi suggests some caution is warranted.

IWM is now 0.75 sigma rich to SPY relative to the macro environment. We tend to wait for Fair Value Gaps to reach 1 sigma before thinking the dislocation versus macro has become overextended. So this is not quite there, but it is starting to get noticeable.

One of the top drivers of the model is FX with a softer Dollar supporting SPY over IWM. A taste of the upcoming earnings season where, after recent Dollar weakness, large cap's international exposure gives them an advantage overdomestically-focused small caps?

Finally, the small cap move does look extended at the global ex US level. SCZ, the iShares ETF tracking MSCI EAFE small caps is now 1.8 sigma (2.1%) rich versus the broader iShares EFA ETF - MSCI EAFE. From a macro perspective, this suggests these aren’t great entry levels to chase small cap outperformance.

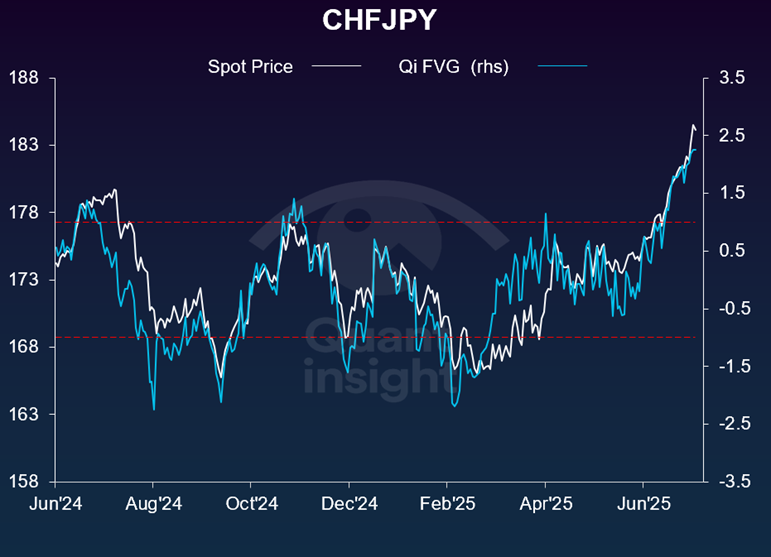

3. CHFJPY – cross asset red flag, or FX idiosyncrasy?

The Swiss franc is now rich versus every G7 currency on Qi’s Fair Value Gap model. The most stretched pair is CHFJPY which is now 2.2 sigma (4.5%) above macro-warranted fair value.

Macro momentum justified CHF gains in April-May. But this latest move has seen spot decouple from macro fundamentals.

When one of the world's main safe havens starts to trade this rich - even versus another classic safe haven - is there abroader message across asset classes? Should equities take heed?

It could simply reflect the search for Dollar alternatives in fx, i.e. it is unique to currency markets with no real read-across to risky assets more broadly.

Either way, CHFJPY looks stretched versus prevailing macro conditions & we note very strong (80%) correlation between spot & Qi's Fair Value Gap over the last year.

The implication being such imbalances have tended to mean revert by the market re-pricing back towards Qi model value.

.png)