The S&P500 in Q2:A Tale of Both Macro & Idio

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

Since the April 8th low, the S&P 500 is up +26% - technically, it’s back in a bull market.

Quant Insight's Risk Model attribution for that return suggests a split of almost two halves:

- 56% macro

- 44% idiosyncratic (the bit macro could not explain)

Relationships are shifting - from a singular focus on the end of US Exceptionalism to Goldilocks Vibes.

Consider the following: In Q1, US equities underperformed. In Q2, it outperformed — despite a weak dollar both times…

So what does Qi's Risk model show:

- Sensitivity to GDP growth = multi-year highs

- Sensitivity to inflation & real rates =multi-year lows

→ Citi US Eco vs. Inflation surprises say itall: growth is holding up, inflation’s cooling

→ Real rates are down 45bps from YTD highs

- Sensitivity to Dollar flipping from positive to now small negative…

Looks like Goldilocks: Fed opening up possibility of cuts, but in a backdrop where growth / inflation trade-off is benign.

Coming up: Trump’s tariff call (July 9) + CPI (week after)

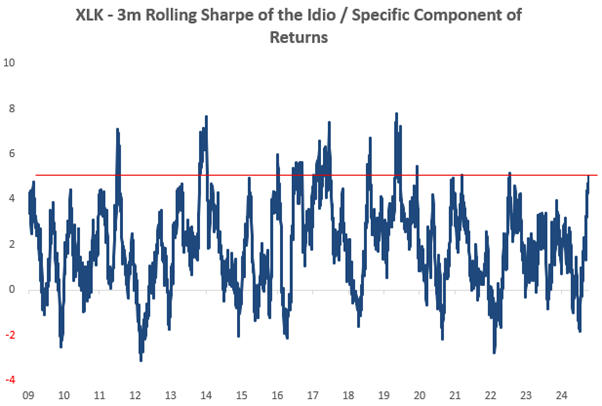

What about that large idio component? US Tech doing its thing

You buy Tech for secular growth, not macro.

Over the last 3months, the idiosyncratic return (what our model can’t explain via macro) forTech (XLK) has jumped dramatically:

- 3M Sharpe of idio component = 5

→ Near the top of its range in recent years

Coming up: Q2 earnings kick off next week, with Tech heavyweights report soon after.

Needless to say, the market pricing provides less of a cushion against disappointment than it did. Our S&P500 Qi total risk indicator is not quite at “macro complacency” but it has climbed a long way from “macro fear”

Charts below.