SPY’s Dynamic Relationship with GDP Growth & Why it Matters Today

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

SPY’s Dynamic Relationship with GDP Growth & Why it Matters Today

The way risky assets react to growth isn’t constant. Markets regularly flip between pricing for growth and pricing for risk.

Plenty of history backs this up:

• 1990s: P/Es tracked Fed policy more than the ISM

• 2009: Massive PE expansion despite negative earnings

• 2012: Draghi’s “Whatever it takes” turned the Eurozone around while it was still in recession

The point: equities discount the future, so PE expansion can offset weak growth data.

This is exactly why Qi’s risk-model framework matters — it helps you spot when markets switch regimes across macro factors.

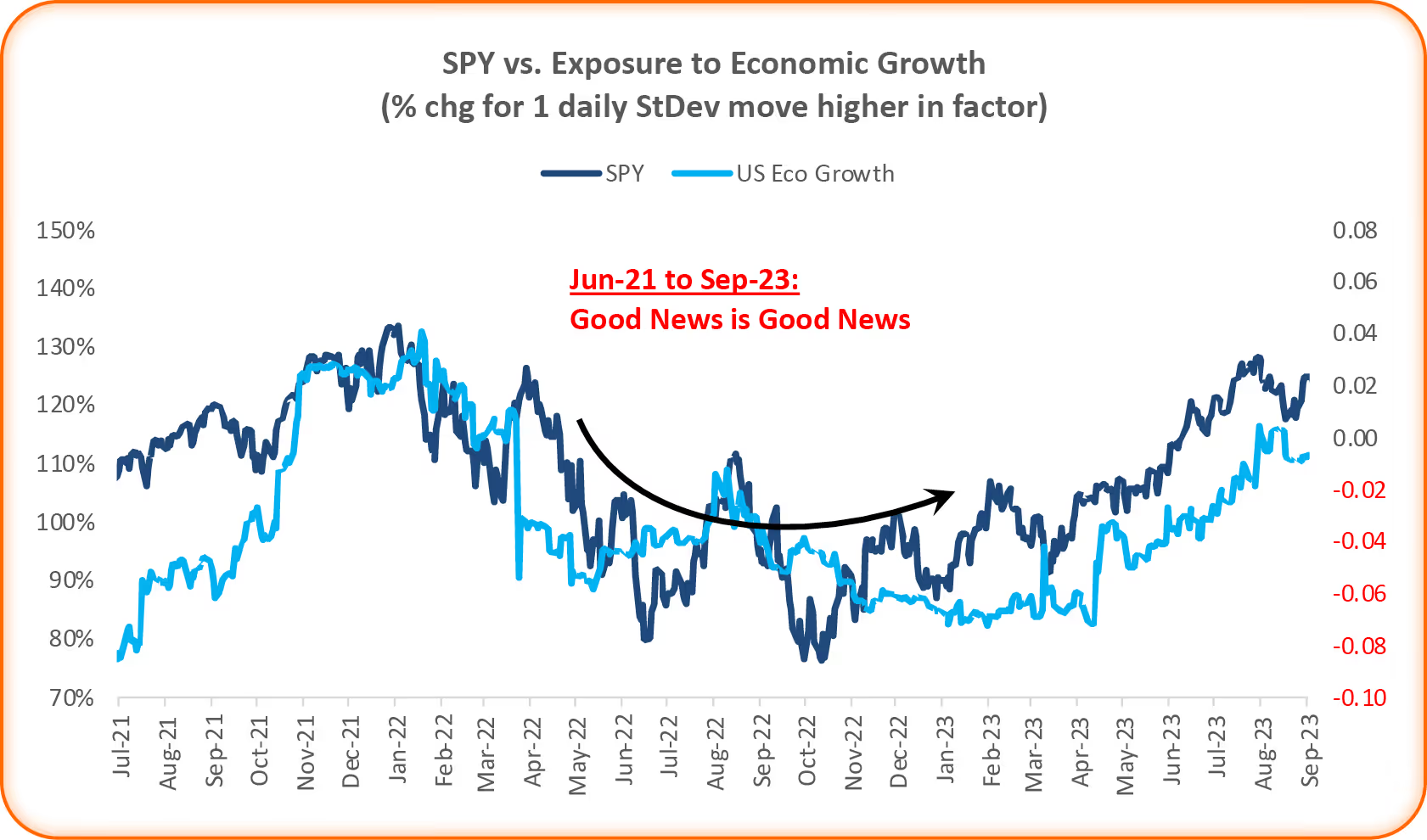

Since 2021, there have been 3 distinct phases in SPY’s relationship with US GDP growth expectations

1. Jun 21 → Sep 23: Good news = good news

A clean macro regime. Stronger GDP → better earnings outlook → supportive for equities.

Continue reading our analysis on the other headlines by downloading the PDF below

Related Articles

Announcement:

Quant Insight brings MFERM to FactSet Portfolio Analytics

The Impact of Rate Vol

.jpg)

Equity Exposures, Sector Trends & Regime Analysis—In Depth

Iran, Oil & the Fed: Who Paid, Who Profited

Crowding Is a Macro Story -Where It Matters