1. Rate sensitive vs. bond proxy stocks – too far, too fast?

2. EURGBP – upside risks

3. EM bonds – trend break or pause that refreshes?

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

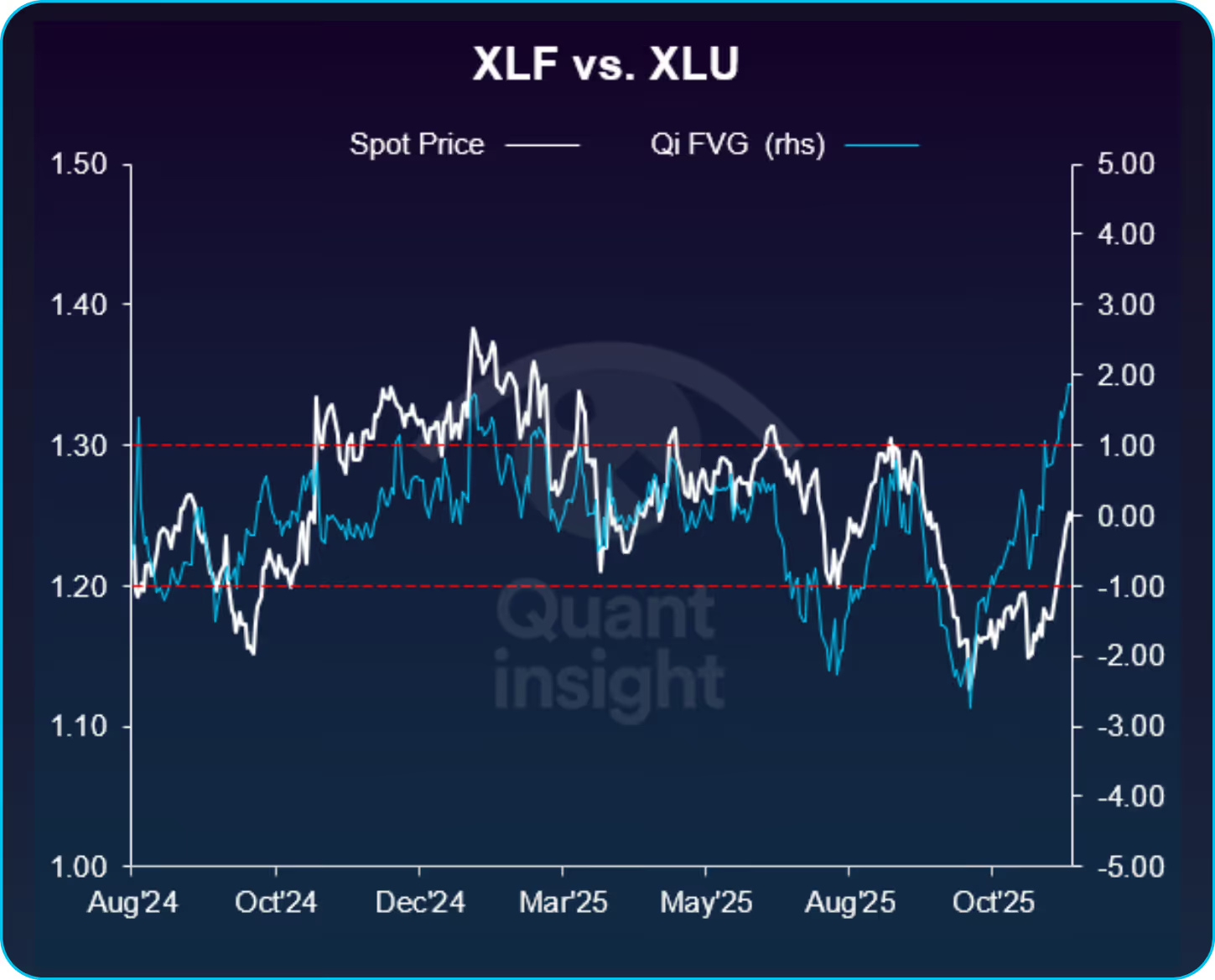

1. Rate sensitive vs. bond proxy stocks – too far, too fast?

The RV pair XLF vs. XLU (US Financials vs. US Utilities) has today a Qi fair value gap of 1.9 sigma / 7.1% rich to its macro-warranted fair value.

Typically this pair has moved with long-end rates given their differing duration features and the recent sell-off in US rates has provided support. US Financials outperformance requires reflationary backdrop where both inflation-expectation and rates move higher. Indeed, it appears the market is excited about growth acceleration in Q1.

However, the fair value gap sits at almost 5yr highs. This must be respected given the close recent correlation with price action and the Qi FVG.

Continue reading our analysis on the other headlines by downloading the PDF below

Related Articles

Identify price dislocations, opportunities, regimes and sensitivities

1. XLF: Running Ahead of Macro Support

2. Sterling looks stretched

3. Tech's Quiet Re-Rating

Identify price dislocations, opportunities, regimes and sensitivities

1. Mag7: Impatience Priced In?

2. EURNOK rally losing macro support

3. US Housing rally runs ahead of macro

Identify price dislocations, opportunities, regimes and sensitivities

1. AI Premium Fades, Macro Discount Still Missing

2. Fading Warsh – 2y Notes

3. Fading Warsh – EURUSD

Identify price dislocations, opportunities, regimes and sensitivities

1. Hang Seng Near Record Cheap vs Macro

2. Falling Inflation, No Value Bid

3. Renaissance IPO ETF - Speculative Risk Is Running Hot