We are now back in the "worry window"

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

The S&P500 is within 3% of all time high, but forward EPS hasn’t budged through the pullback or the bounce.

That’s the worry window: price up but earnings estimates potentially start to bleed.

Now throw in this:

Trump tells Walmart to “eat the tariffs”

If Walmart is saying it has to raise prices what will smaller retailers do who are less able to negotiate better prices? So do corporate profit margins now need to absorb the impact of trade policy??

Furthermore, we are about to enter a confusing period of likely conflicting soft vs. hard data The implication is that earnings momentum will be key in separating winners from losers.

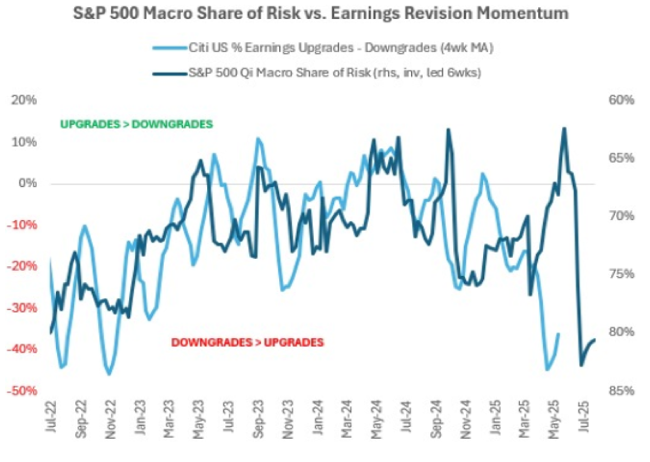

Let’s benchmark this using Qi’s Risk Model:

The below chart shows the 4wk moving average of % earnings upgrades vs. downgrades for the S&P 500 vs. Qi’s Macro Share of Risk for the index.

There is an inverse & slightly leading relationship: High macro share of risk = high uncertainty on the distribution of outcomes = less confidence to upgrade earnings estimates. At this time, it still looks like earnings are more likely to bleed than bounce.

The challenge will be for stocks to look through that.