Momentum is heading into a higher vulnerability regime.

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

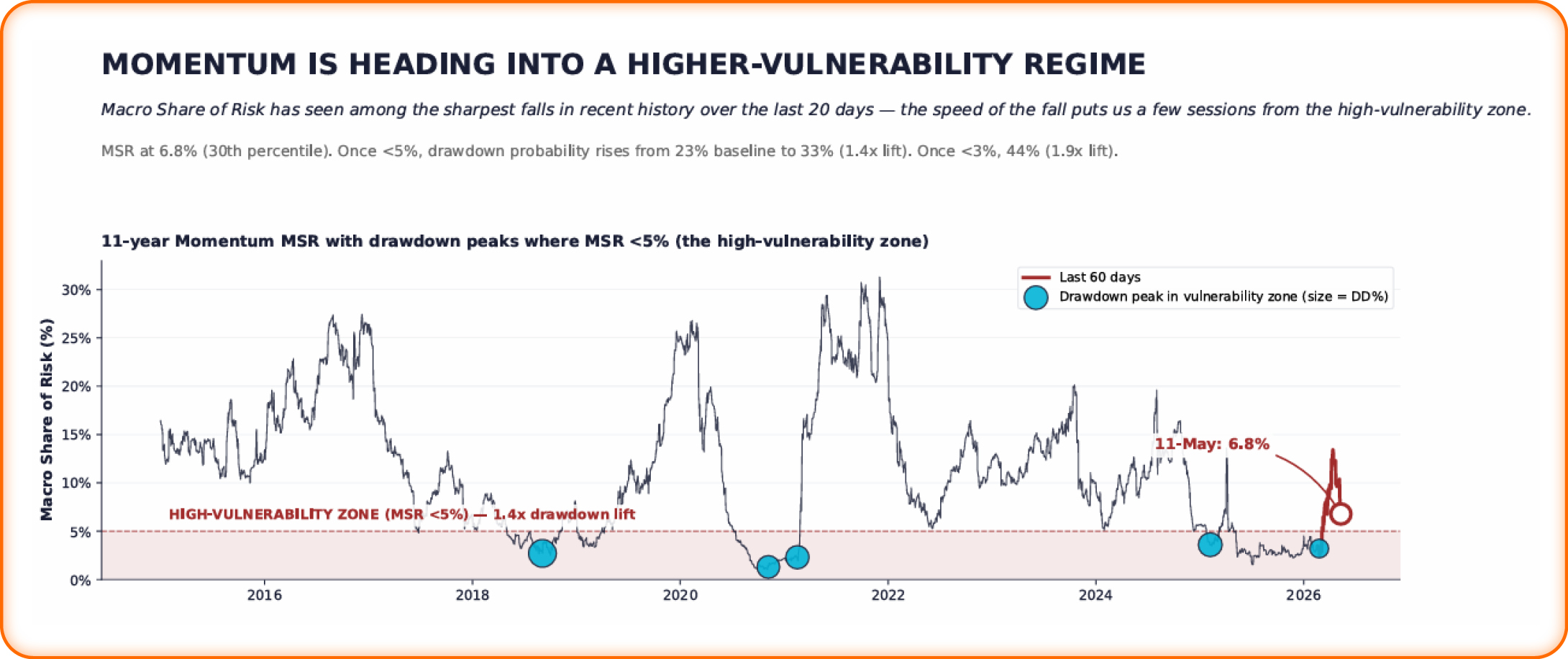

Momentum is heading into a higher vulnerability regime.

Quant Insight’s MFERM model decomposes asset risk into macro and idiosyncratic components. The ratio of the two — Macro Share of Risk — has fallen from 13.4% to 6.8% on Citi’s Pure Momentum index over the last 20 sessions.

That is a bottom 4% 20-day contraction over 11 years.

The macro footprint in Momentum is draining out of the price.

Why it matters:

- MSR <5%: drawdown probability rises from 23% baseline to 33%

- MSR ≤3%: drawdown probability rises to 44%

- MSR >20%: drawdown probability falls to 9%

The relationship is monotonic: the lower MSR goes, the wider the return distribution becomes...

This matters for the live debate on how to hedge Momentum.

Continue reading our analysis by downloading the PDF above

Related Articles

Announcement:

Quant Insight brings MFERM to FactSet Portfolio Analytics

The Impact of Rate Vol

.jpg)

Equity Exposures, Sector Trends & Regime Analysis—In Depth

Iran, Oil & the Fed: Who Paid, Who Profited

Crowding Is a Macro Story -Where It Matters