Oracle. The credit signal moved first.

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

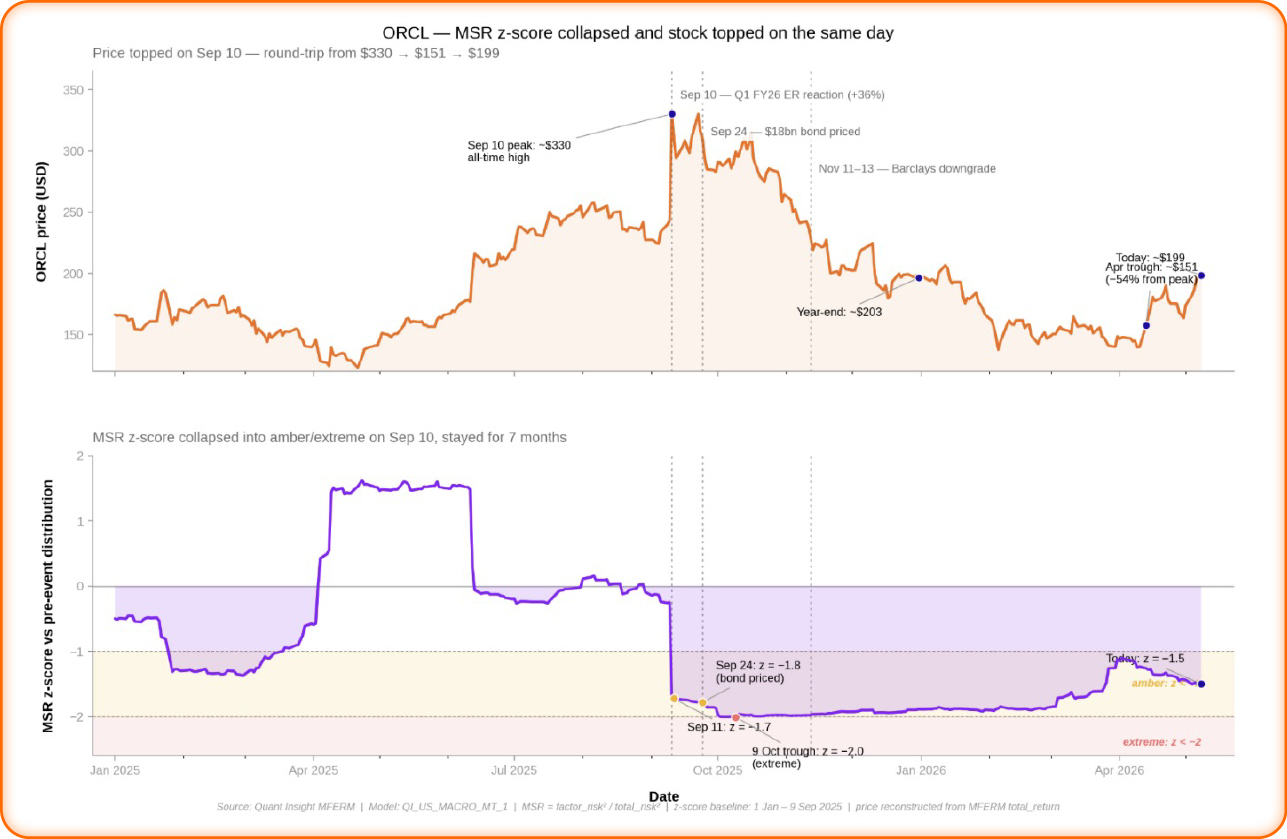

Oracle. The credit signal moved first.

September 2025. MFERM flagged Oracle’s rising corporate credit sensitivity before the $18bn bond priced. Before the street downgrades. Before the consensus caught up.

Not a prediction. A measurement.

On Sep 10, Oracle reported blowout earnings. The stock hit $330, an all-time high. Two weeks later, Oracle priced $18bn of debt, one of the first mega-cap tech names to fund AI capex through bond markets rather than free cash flow.

Seven weeks after that, Barclays downgraded. The stock was already rolling over. The round trip: $330 to $151, down 54%.

What MSR was telling you

The same day earnings hit, Qi’s Macro Share of Risk collapsed to a z-score of -1.7. Idiosyncratic risk was overwhelming macro in the vol mix; the condition we associate with macro complacency. A stock priced on fundamentals alone, blind to building macro risk.

Continue reading our analysis by downloading the PDF above

Related Articles

The Impact of Rate Vol

.jpg)

Equity Exposures, Sector Trends & Regime Analysis—In Depth

Iran, Oil & the Fed: Who Paid, Who Profited

Crowding Is a Macro Story -Where It Matters

Equity Exposures, Sector Trends & Regime Analysis—In Depth

The market has stopped pricing credit risk.