1. S&P 500 - Same Data, New Regime

2. Rotation Risk: QQQ Looks Stretched vs IWM

3. Re-visiting FX carry

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

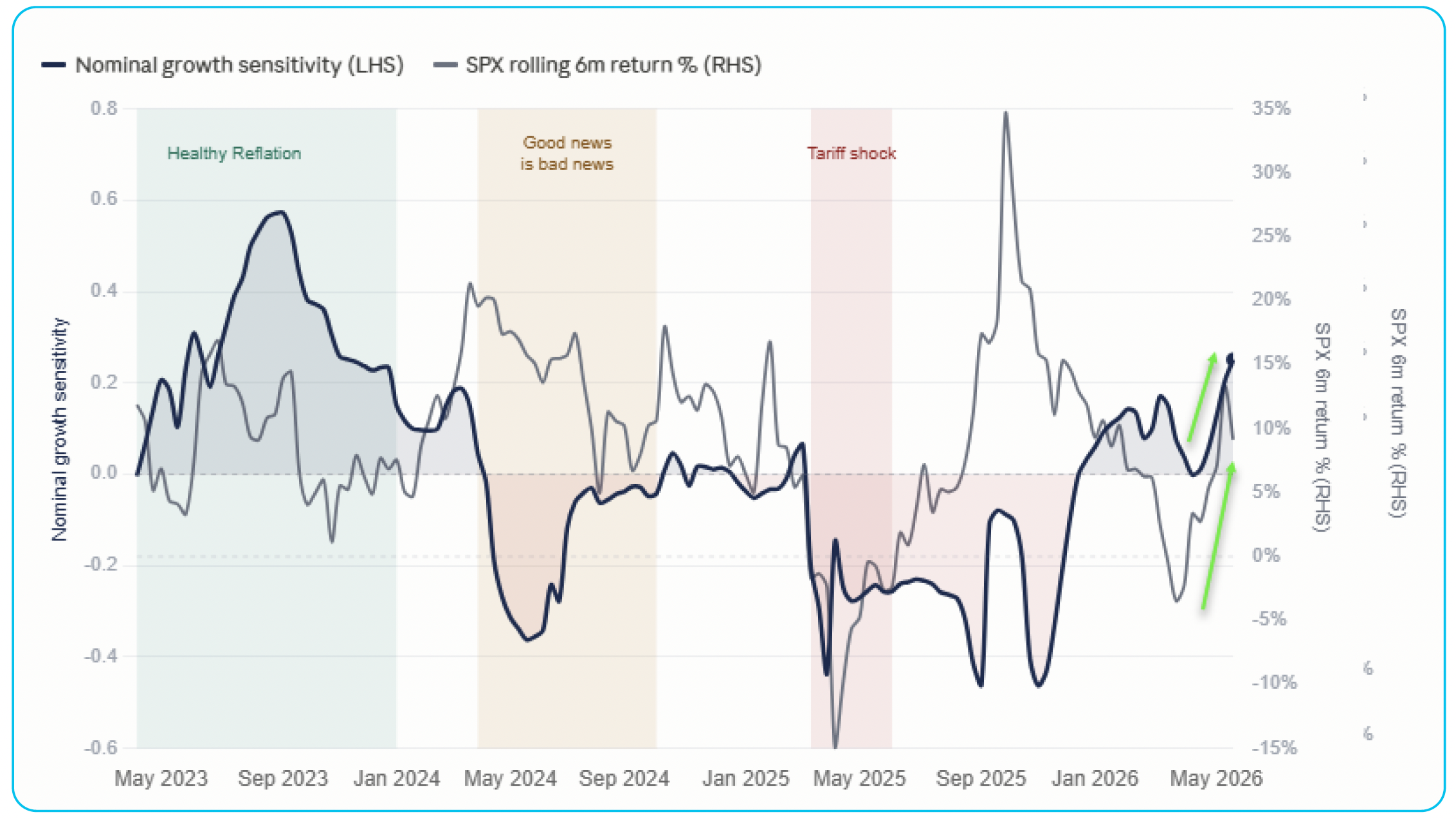

S&P 500 - Same Data, New Regime

S&P500’s exposure to nominal US growth – combining Qi’ssensitivity to tracking US GDP growth & 5y US inflation expectations – hashit its highest in 2 years. The chart captures four distinct regimes:

2023. Healthy Reflation. As the Fed tightening cycleended, sensitivity recovered. Markets re-embraced inflation as a growth signal.SPX followed.

Early 2024. Good News is Bad News. Strong data pushedback rate cut expectations. Higher nominal growth hurt rather than helped.Sensitivity went negative.

Q1 2025. Tariff Shock. Sharp but short-lived. Marketsfeared an inflation shock, not growth. Sensitivity collapsed. SPX sold offhard.

Today. Sensitivity is back at 2-year highs. With theIran risk premium fading and the tariff shock absorbed, US equities arere-pricing the macro backdrop. The emerging regime sees nominal growth as atailwind, not an inflation risk or rate risk.

The post Iran energy shock has given way to a domestic USgrowth story.

Continue reading our analysis by downloading the PDF above

Related Articles

Identify price dislocations, opportunities, regimes and sensitivities

1. S&P 500 - Same Data, New Regime

2. Rotation Risk: QQQ Looks Stretched vs IWM

3. Re-visiting FX carry

Identify price dislocations, opportunities, regimes and sensitivities

1. Equity bears need a Plan B?

2. Poor risk-reward in credit

3. Bonds vs Commodities: more to give

Identify price dislocations, opportunities, regimes and sensitivities

1. Cyclicals are at new highs. Macro isn’t there yet.

2. Europe HY Looks the Vulnerable Trade

3. QQEW: The One Still in Regime

Identify price dislocations, opportunities, regimes and sensitivities

1. KWEB looking interesting again, especially vs. FDN

2. USDJPY: Intervention Can Slow It. Not Stop It.

3. TU: Cheap Enough to Matter Again