1. Small Caps vs. Large Caps & Real Rates

2. EURNOK - cheap "riskoff" hedge

3. Tactical Asset Allocation update

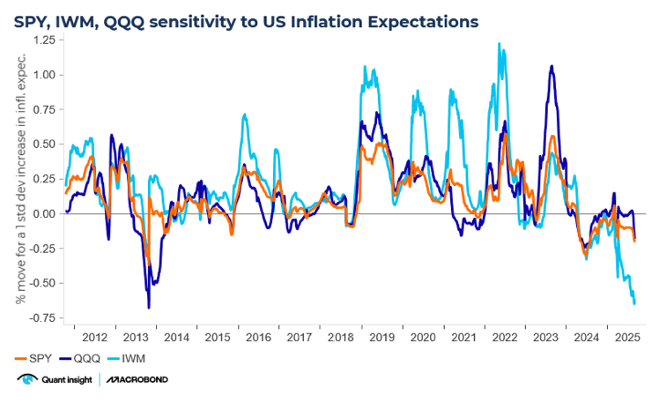

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

1. Small Caps vs. Large Caps sensitivity to real rates at multi-year extremes

It is well acknowledged that small-cap stocks react more sharply to changes in real interest rates: more rate-sensitive, credit-sensitive, and valuation-sensitive than large caps. Front-loaded cash flow, less pricing powerand a poor earnings profile implies their valuation is more sensitive to financial conditions.

However, with real rates reaching their 95th percentile over the last 10yrs, that relationship has hit multi-year extremes. Real rates remain the critical driver of the relative performance of IWM vs. SPY

2. EURNOK – cheap “risk off” hedge

Thus far, the Norges Bank has been an outlier amongst G10 Central Banks - it is the only one not to have started a rate cutting cycle. But this week Norwegian CPI fell back to the lows of 2025 seen back in January. Markets hope benign inflation will prompt a first reduction at September's meeting.

On Qi, the ECB -Norges Bank policy stance isn't the key driver; EURNOK's sensitivity tointerest rate differentials is modest. The bigger driver is Risk Aversion,which explains 40% of model variance.

And that's the keypoint - the move lower hasovershot given VIX is now back below 20. The cross sits almost 1 sigma cheap tomodel. There are two health warnings - EURNOK is not in a macro regime and model value is falling. But for anyone looking for efficient "risk off" hedges, EURNOK upside looks attractive, especially given Qi's FVG has done a good job of capturing local turning points in spot.

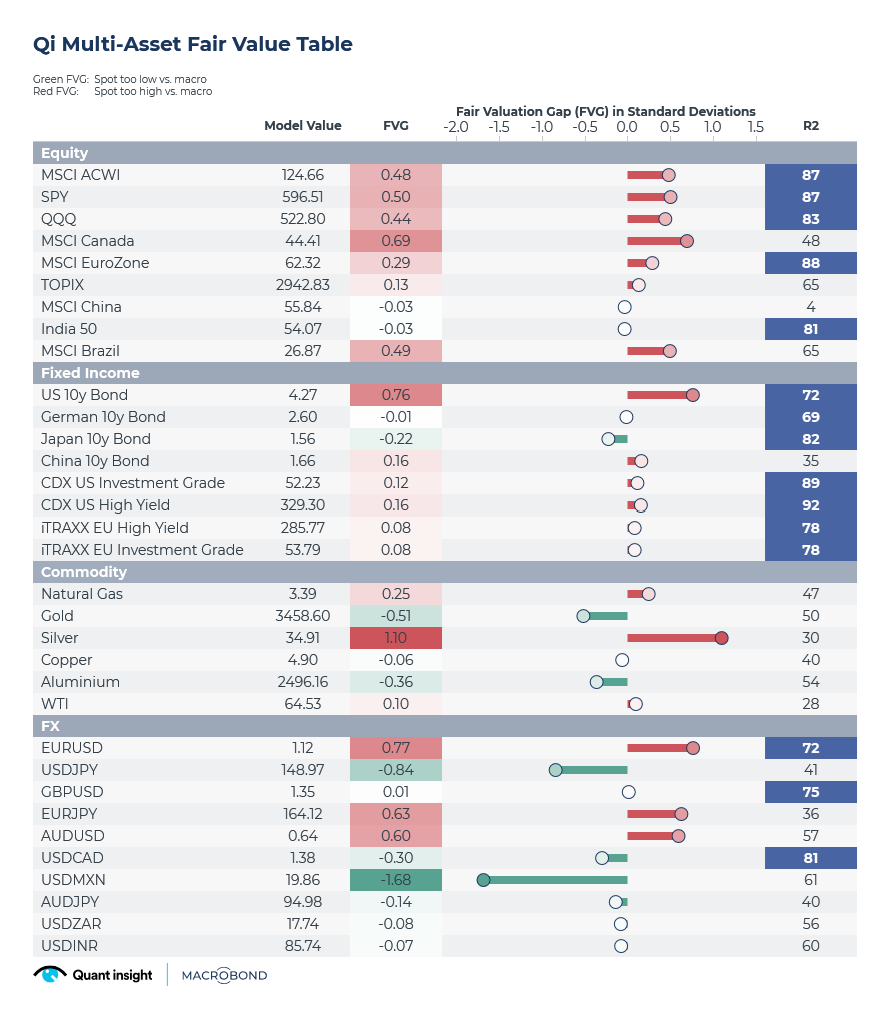

3. Tactical Asset Allocation update

As we approach the half way point of the year, what does the global multi-asset picture look like from Qi's perspective? Macrobond's best-in-class charts help in this regard.

· most global equity markets are rich to aggregate macro conditions but only modestly so. China is the outlier but macro isn't the key driver there. India is in regime and alaggard worthy of bull's attention.

· most Fixed Income models are in macro regimes and close to fair value. The outlier is 10y US Treasuries. The FVG isn't yet sufficient to fire a bullish signal but it is incheap territory on Qi.

· not a single commodity model is in regime right now. Geopolitics & trade wars matters more?

· in FX, the dominant pattern is the US Dollar which screens as cheap to various degrees. Yes there are strong arguments for asecular regime change in currency markets - one where capital flows trump traditional interest rate differentials. But it is interesting to note macro explanatory power generally remains decent.

· USDMXN is the standout FVG. These are rare levels - the cross has only been this cheap on Qi on four occasions in the last 15 years. In three of those four instances, the FVG was resolved by the market catching up with Qi's macro-warranted model value.

.png)