1. Risk Appetite stalling

2. EURGBP overdone; GBPCHF offers better risk-reward?

3. Lock-incommodity equity gains

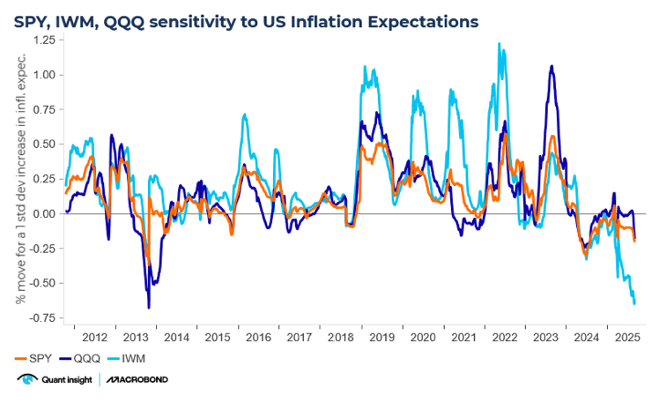

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

1. Risk Appetite stalling

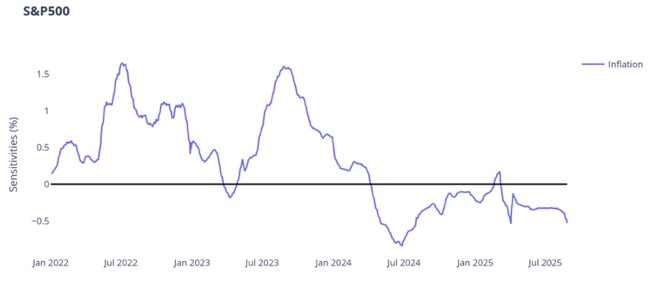

S&P500 spot and Qi model value have been range-bound through June. With S&P500 forward multiples reaching close to 22x, the concern is we have already climbed the‘wall of worry’.

This concern is being reflected in the S&P 500’s Qi sensitivity to risk aversion. Intuitively, when fear is high, we would expect the index to be highly sensitive to rises in VIX; in contrast, when there is greed, sensitivity would likely be low. And this is indeed what we see in the chart below.

As the sensitivity to higher VIX diminishes toward positive territory, risk appetite is rising. We highlight points of market vulnerability at the upper end of the historical range e.g. Nov-21, Jul-23, Jul-24 and Mar-25. Today, while we are not quite in positive territory, sensitivity to VIX has been diminishing through April and now looks to be stalling.

2. EURGBP overdone; GBPCHF offers better risk-reward?

EURGBP recently entered a new macro regime where credit and inflation differentials are the main drivers. The Euro is a safe haven asset outperforming when credit spreads widen, but also benefits from future growth prospects (positivesensitivity to inflation differentials means European reflation helps the single currency).

EURGBP now sits 1.4 sigma (1.5%) rich to Qi's macro-warranted model value. That's a fairly elevated FVG by recent historical standards.

For those looking at Sterling upside but who don't want to fight the upward momentum in the Euro,an alternative trade expression would be GBPCHF which screens 1.1 sigma cheapon Qi.

There are strong reasons- Middle East tensions; alternative safe havens for reserve managers - to believe both the Euro and Swiss Franc are undergoing a secular re-rating. But there will be tactical opportunities to finesse that trade and it is worth noting:

· Hedge Funds are running their longest net long position in Swissy in almost 4 years according to TIFF data.

· a -1.1sigma FVG elicits a strong hit rate - 73% with no RSq constraint, 88% when in regime.

· strong (81% over the last year) correlation between spot GBPCHF and Qi FVG suggests the "right" kind of mean reversion.

3. Lock-in commodity equity gains

Evidently the rise in geopolitical risk can be seen in the rally in gold and oil. The fact that Trump wants lower oil prices is well known and the assumptionis Saudi Arabia will increase production if Iranian action escalates.

The GS US commodity basket tracks companies exposed to energy, metals (industrials and precious) and agricultural commodities. It has rallied ~32% from the April lows.

Qi’s analytics show it is trading 1.9 sigma above Qi model value. That is close to multi-year highs. The basket spot price has been tracking this fair value gap closely over the last 1yr i.e. we should be on the lookout for mean reversion from extended levels.

Qi is saying the gains should be now lockedin.

.png)