US Homebuilders - TOL

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

To date, the dominant question during Q2 results season has been how Trump's tariffs have impacted company earnings. Given the Moody's news, the focus could shift to how corporate America fares with higher bond yields. Homebuilders will always be a closely watched sector in this regard & tmrw after the close Toll Brothers report.

The stock has had a tough 6 months & macro factors have played an important role. They helped mitigate some of the downside in Q1... added to the downside momentum around the early tariff announcements... have been the driving force behind the recovery over the last month.

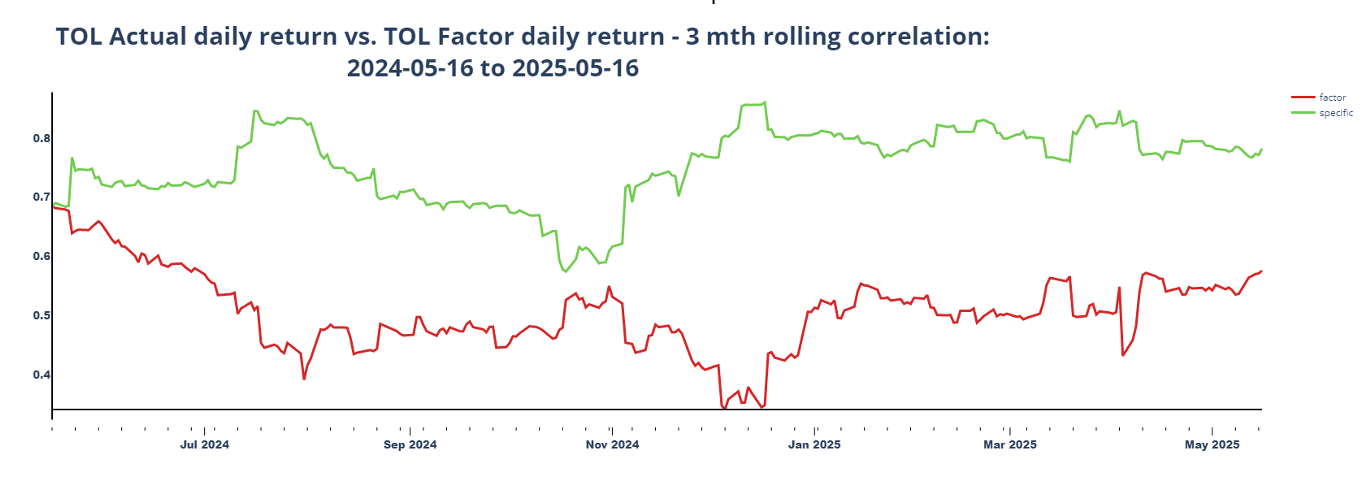

Macro's rising importance can be seen with its correlation to actual returns at recent highs.

Intuitively you'd expect a house builder to want lower interest rates & Qi confirms exposure to both nominal & real rates is negative. But its actually credit that screens as the dominant macro factor exposure.

Yes, equity investors need to be watching the Fixed Income market - not just rates, but HY credit spreads as well.

These exposures are - as you'd expect - amongst the highest. Looking across GICS L1 sectors we can see TOL is

> more reliant on HY spreads tightening

> more vulnerable should nominal & real yields leg higher still