US Small Caps: Sharpe at Multi-Year Highs — Macro Tailwinds or Complacency?

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

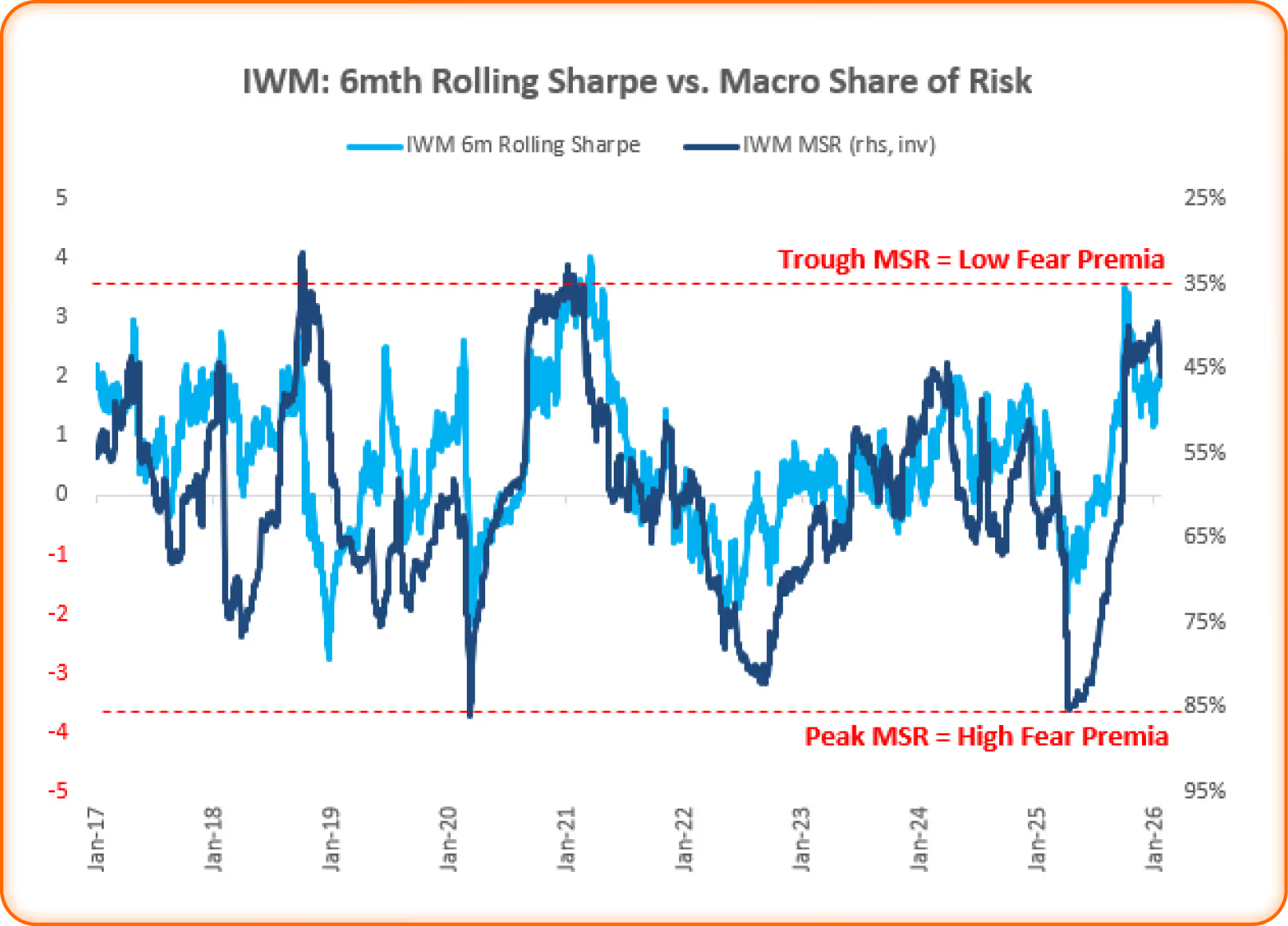

Into year-end 2025, the Sharpe ratio of IWM (US small caps) hit multi-year highs.

Why? Quant Insight’s Risk Model helps unpack it:

Macro Share of Risk (MSR) for IWM hit multi-year highs in Apr’25, then fell to range lows by Jan’26 — a signal of dissipating macro fear translating into a tailwind for risk-adjusted returns.

Continue reading our analysis on the other headlines by downloading the PDF below

Related Articles

.jpg)

Equity Exposures, Sector Trends & Regime Analysis—In Depth

Iran, Oil & the Fed: Who Paid, Who Profited

Crowding Is a Macro Story -Where It Matters

Equity Exposures, Sector Trends & Regime Analysis—In Depth

The market has stopped pricing credit risk.

Equity Exposures, Sector Trends & Regime Analysis—In Depth

Dollar up, stocks down. It's not that simple.