Same framework. Different factor. Opposite risk signal.

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Same framework. Different factor. Opposite risk signal.

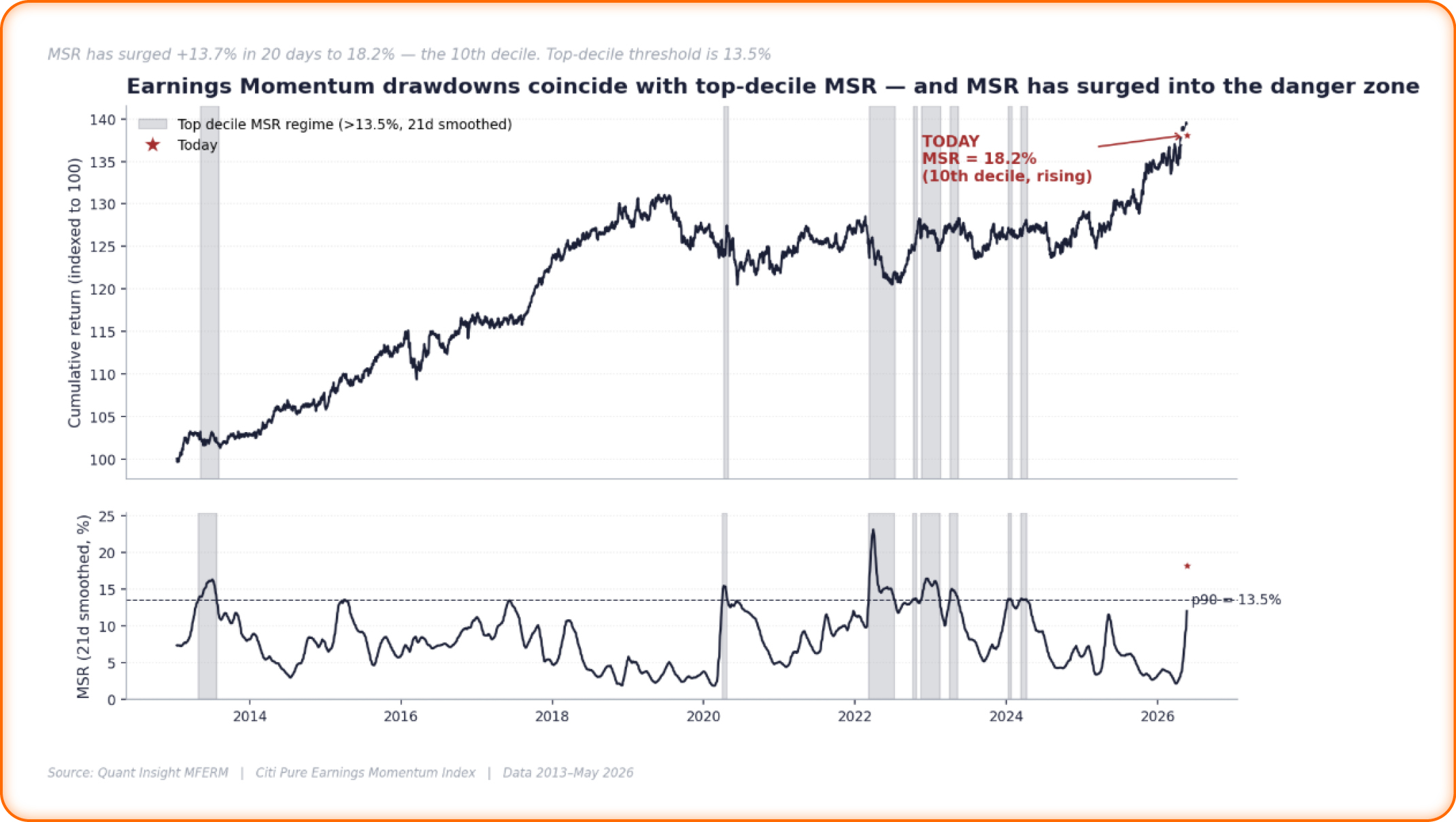

Two weeks ago, Qi flagged drawdown risk in Momentum via MSR.

Today the same framework is flagging a different factor — Earnings Momentum — but for the opposite reason.

MSR measures how much of a factor’s return variance is being explained by macro. But different factor archetypes are vulnerable in different MSR regimes.

For Price Momentum, low MSR is the fragility zone. Macro influence fades, idiosyncratic price action dominates, crowding builds in the winners — and the next macro shock can unwind the trade.

For Earnings Momentum, the risk is the other way around.

Continue reading our analysis by downloading the PDF above

Related Articles

.jpg)

Equity Exposures, Sector Trends & Regime Analysis—In Depth

Same framework. Different factor. Opposite risk signal.

Equity Exposures, Sector Trends & Regime Analysis—In Depth

Momentum is heading into a higher vulnerability regime.

Equity Exposures, Sector Trends & Regime Analysis—In Depth

Oracle. The credit signal moved first.

.jpg)

Equity Exposures, Sector Trends & Regime Analysis—In Depth

SOXX in 2026: The AI Narrative is Real. But It’s Not the Whole Story.