1. When De-escalation meets Recession

2. The Walmart Indicator

3. NOKSEK – From Momentum to Mean Reversion

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

1.When De-escalation meets Recession

This week has seen equities follow the post Liberation Day playbook. But at some point, the risk is this relief rally bumps up against other narratives - high energy/food prices, a Fed “policy error”, a recession.

Investors are left trying to navigate the fear of being caught short in any de-escalation rally, versus longer term fundamental concerns for the economy.

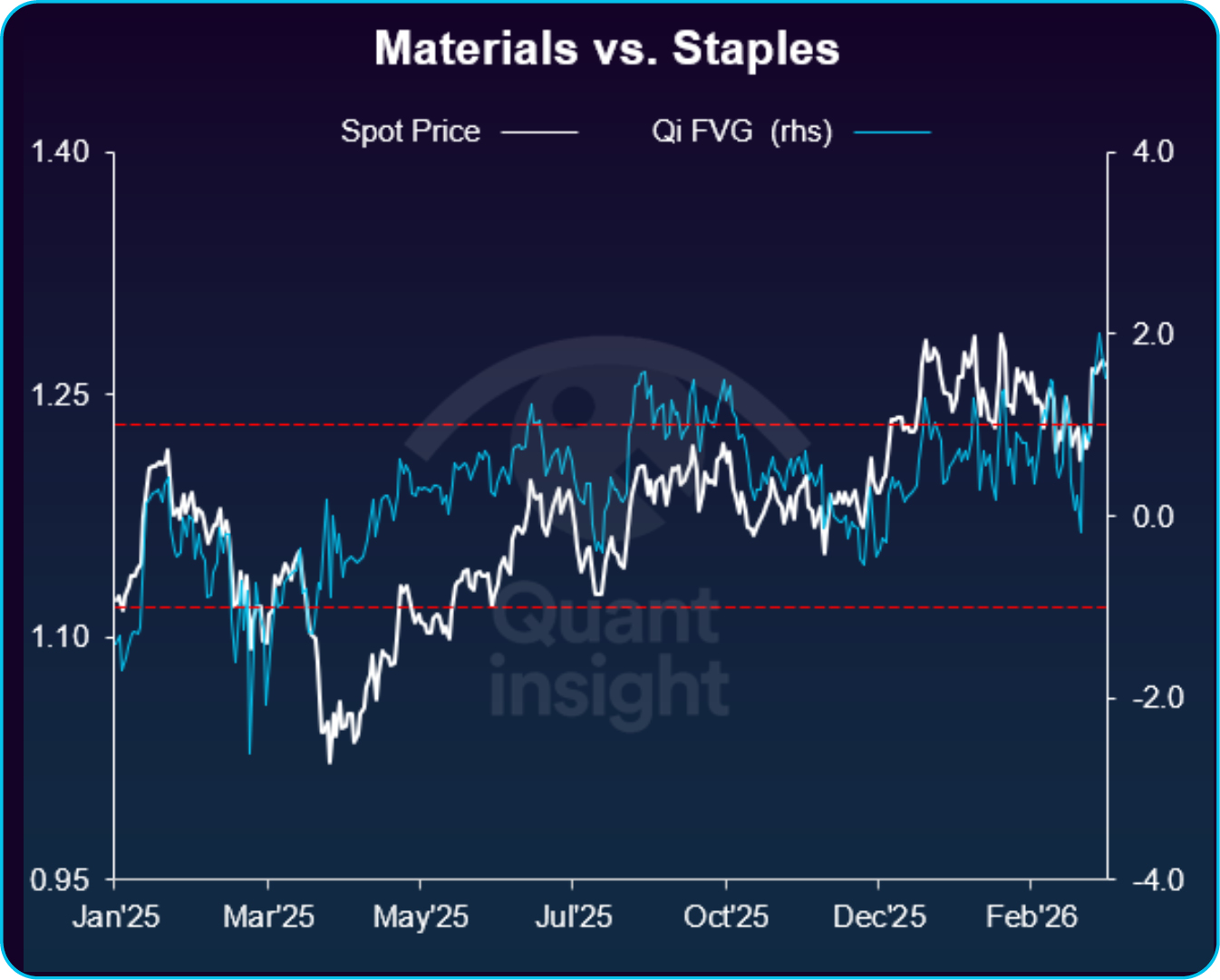

At the sector level, Materials are the second-best performing sector in the S&P500 YtD, up 9.3%. The long-term prognosis is positive but, for the tactically minded, the sector could be vulnerable to profit-taking in a de-escalation scenario. Staples have also fared well, but increased recession fears would probably add extra momentum.

Qi shows Materials outperform on higher energy, a stronger Dollar, a hawkish Fed that bear flattens the yield curve. All that has transpired but Materials have overshot & now screen as 1.5 sigma (4.6%) rich to Consumer Staples. That’s towards the top end of recent FVG ranges, & recent correlations point to the “right” kind of mean reversion.

Continue reading our analysis by downloading the PDF above

Related Articles

Identify price dislocations, opportunities, regimes and sensitivities

1. GS HF VIP vs. VIP Short: Crowding Stress

2. Heavy AI Issuance Creates a Contrarian Credit Opportunity

3. ChiNext: the tape and the model have parted ways

Identify price dislocations, opportunities, regimes and sensitivities

1. US Metals & Mining

2. China vs. India

3. NZDCHF

Identify price dislocations, opportunities, regimes and sensitivities

1. XLF: Running Ahead of Macro Support

2. Sterling looks stretched

3. Tech's Quiet Re-Rating

Identify price dislocations, opportunities, regimes and sensitivities

1. Mag7: Impatience Priced In?

2. EURNOK rally losing macro support

3. US Housing rally runs ahead of macro