1. US equities resemble Wile E. Coyote

2. Credit is cracking, credit-sensitive equities aren’t

3. Crude Oil’s Currency Playbook

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

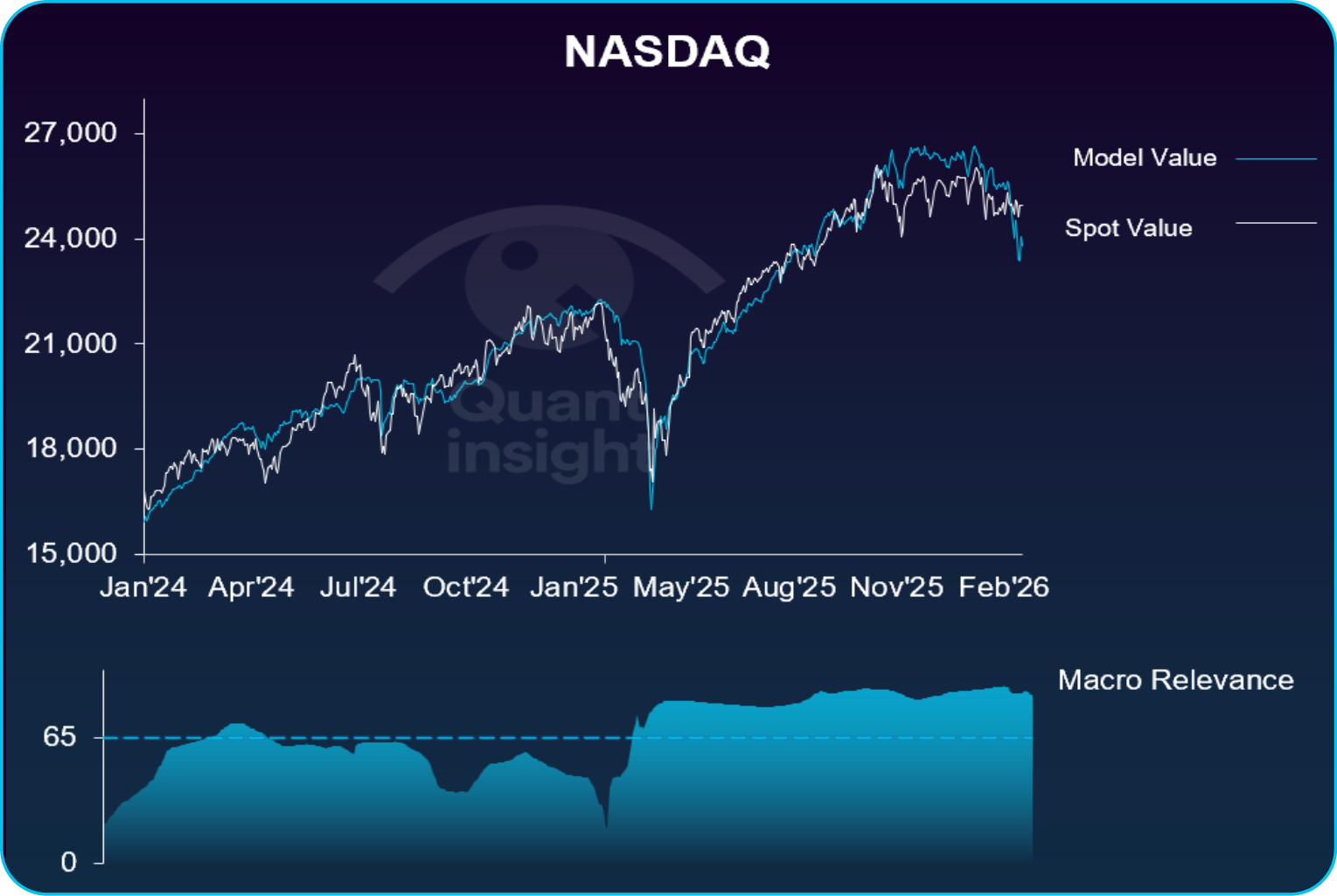

US equities resemble Wile E. Coyote

Both the S&P500 and NASDAQ are around 1 sigma rich.Since the conflict in Iran began, Qi’s macro-warranted model value has fallen5.5% for the former, nearly 7% for the latter.

The big driver pushing Qi model value lower is the movewider in credit spreads & the rise in interest rate volatility. Equitiesare lagging this tightening of financial conditions.

This bearish divergence shifts the risk-reward in US equities to the downside. Other forces (chart support?) may help explain equities relative resilience. But note macro explains 90% and 87% of the S&P500 and the NASDAQ respectively.

Continue reading our analysis on the other headlines by downloading the PDF below

Related Articles

Identify price dislocations, opportunities, regimes and sensitivities

1. GS HF VIP vs. VIP Short: Crowding Stress

2. Heavy AI Issuance Creates a Contrarian Credit Opportunity

3. ChiNext: the tape and the model have parted ways

Identify price dislocations, opportunities, regimes and sensitivities

1. US Metals & Mining

2. China vs. India

3. NZDCHF

Identify price dislocations, opportunities, regimes and sensitivities

1. XLF: Running Ahead of Macro Support

2. Sterling looks stretched

3. Tech's Quiet Re-Rating

Identify price dislocations, opportunities, regimes and sensitivities

1. Mag7: Impatience Priced In?

2. EURNOK rally losing macro support

3. US Housing rally runs ahead of macro