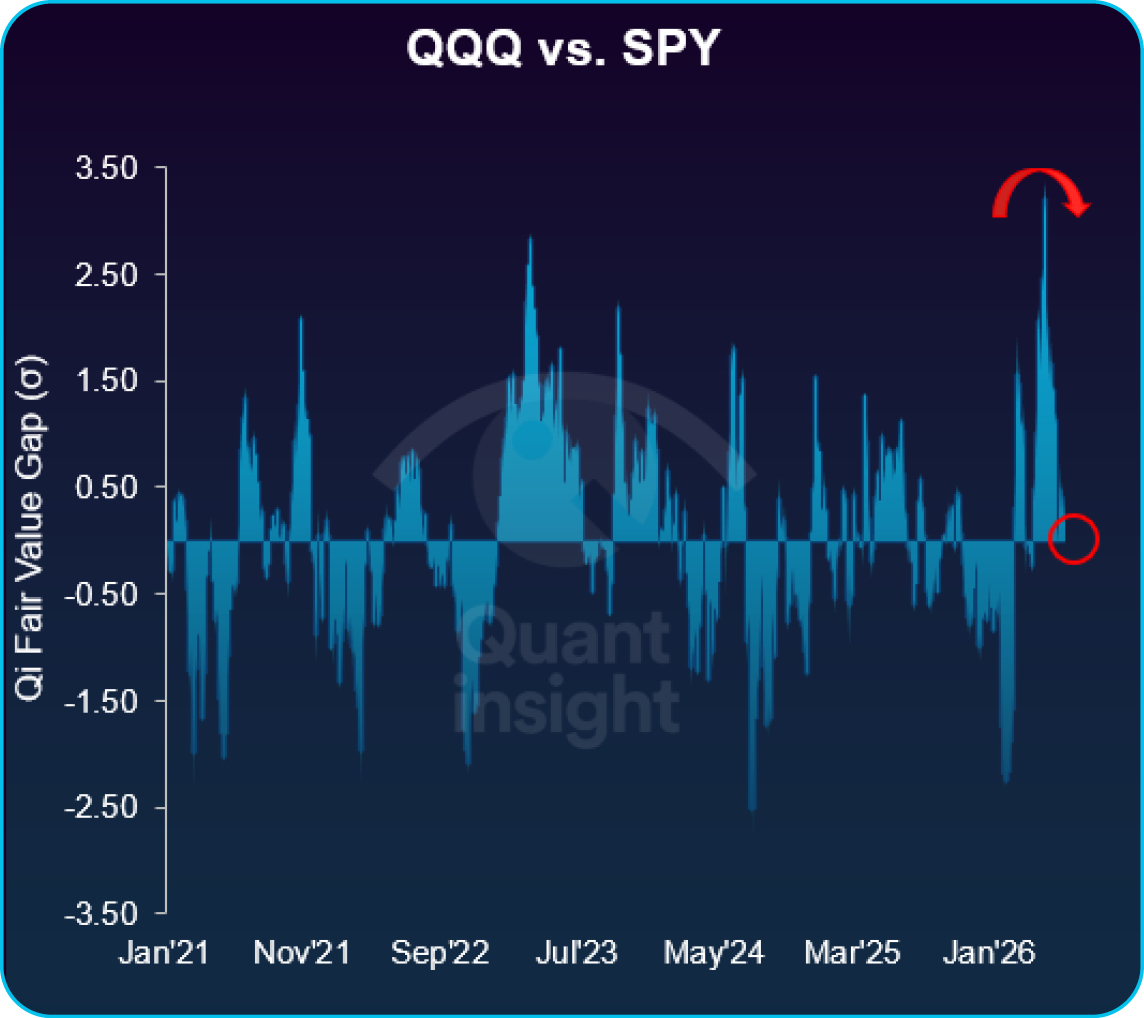

1. AI Premium Fades, Macro Discount Still Missing

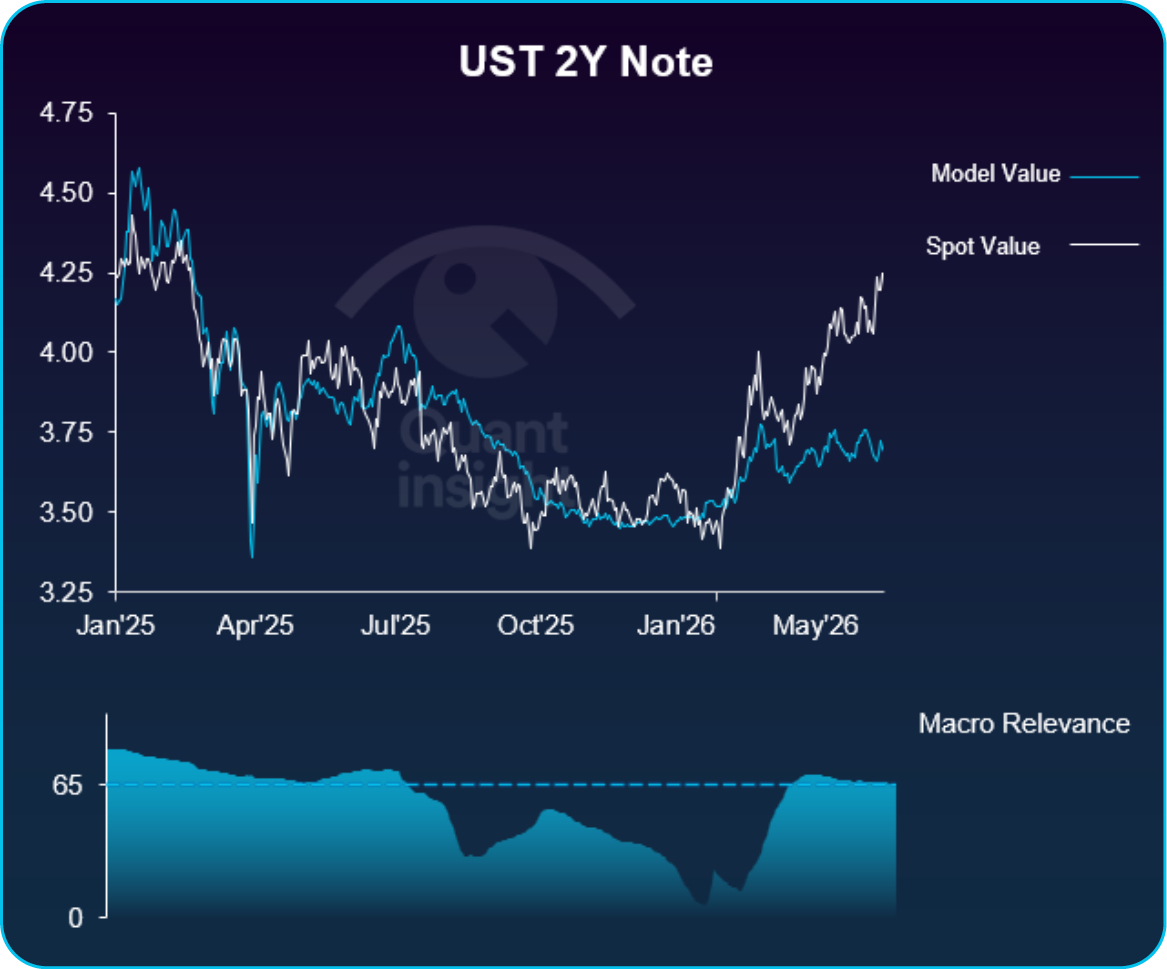

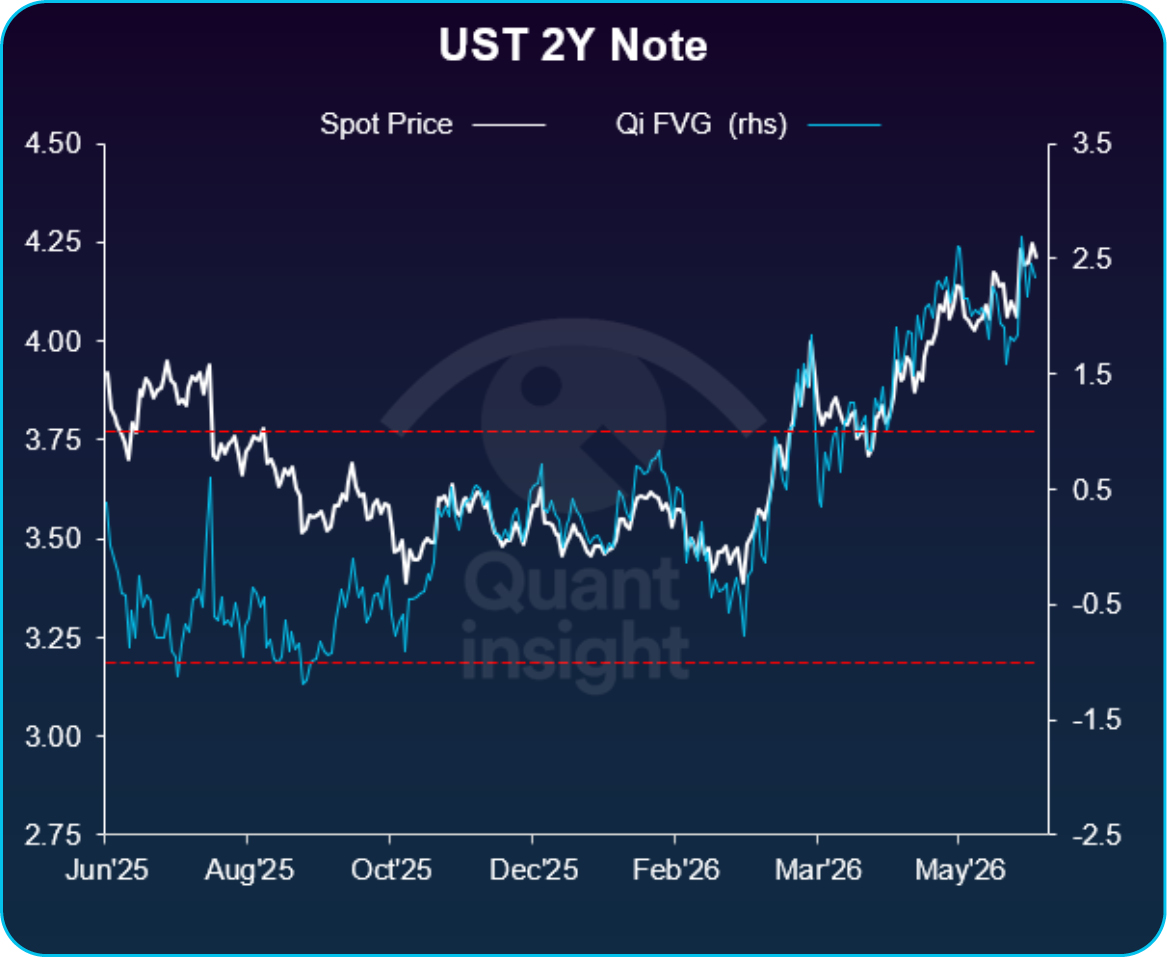

2. Fading Warsh – 2y Notes

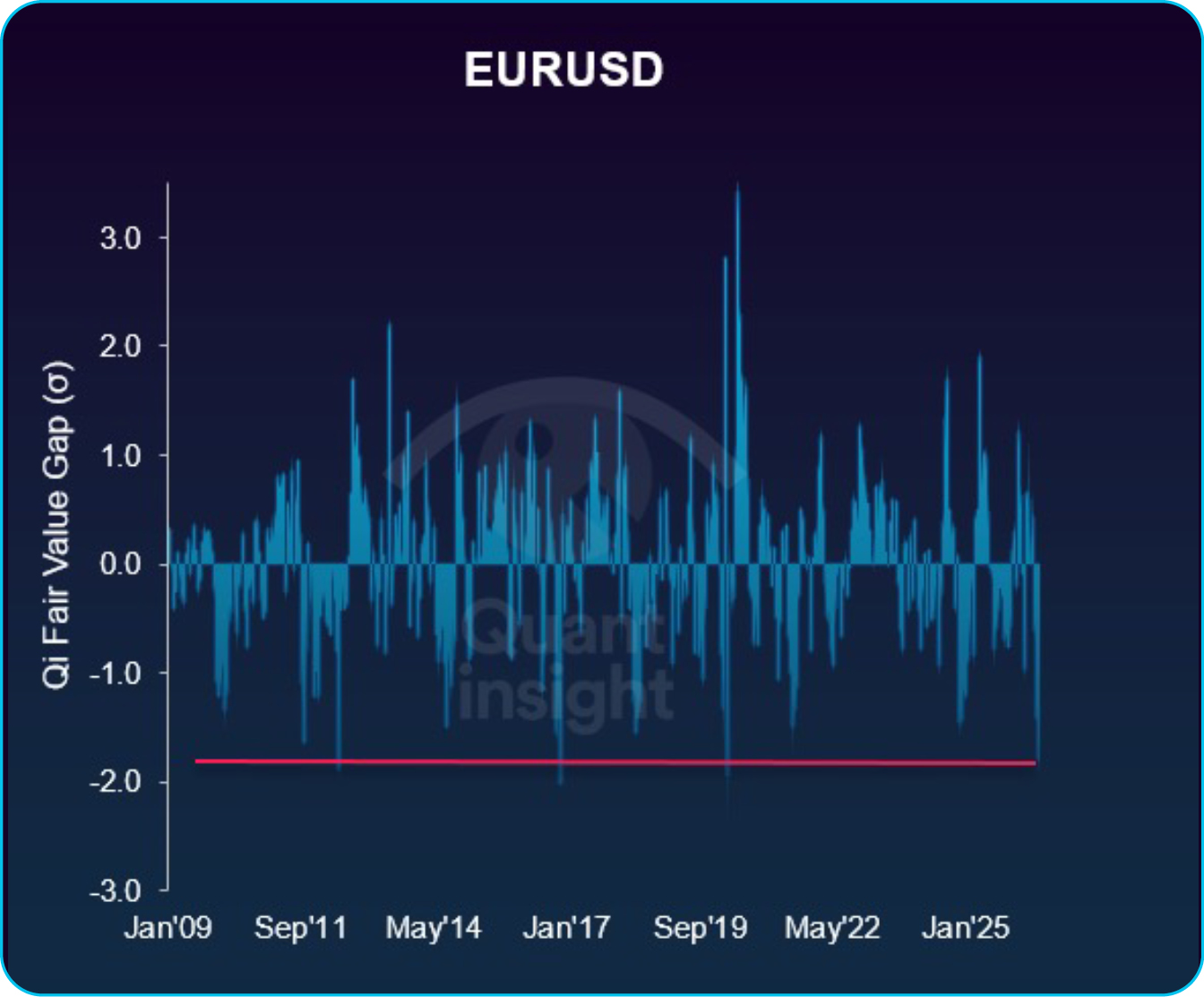

3. Fading Warsh – EURUSD

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

1.AI Premium Fades, Macro Discount Still Missing

Recent US equity weakness has been narrow, not broad. SPY is down around 3% from peak, but equal-weight S&P is only off 1.5%. QQQ is down 4.3% from its June high - a leadership correction, not a broad equity unwind.

Qi had already flagged the risk. From mid-May, SOXX and QQQ started to screen rich versus SPY as AI/tech narratives took hold. That relative exuberance has now faded. But the key point is this: Qi model value is broadly neutral to spot.

So, the premium has compressed, but a macro discount has not opened up.

The macro factor mix also matters. SOXX and QQQ still want a benign backdrop: flatter 5s30s, tighter credit spreads, lower risk aversion and firmer inflation expectations.

It wants “reflation without stress” — resilient nominal growth, easier financial conditions and contained volatility.

Bottom line: tech led the squeeze higher, and tech is leading the correction. The AI premium has been reduced, but these assets are not yet cheap to macro.

2. Fading Warsh – 2y Notes

The sharp rise in 2y US Treasury yields since last week’s FOMC has opened a +2 sigma Fair Value Gap on Qi. The market read Warsh as hawkish & re-priced, but Qi puts macro-warranted fair value around 3.70% thanks mainly to the fall in inflation expectations.

If your Fed watching conclusion is Warsh leans hawkish, this signal can safely be ignored. Just be aware macro relevance is high (65%) &, over the last 9mths, the correlation between spot 2y yields & Qi’s FVG is very strong suggesting the mean reversion has occurred via the market re-pricing to macro conditions.

3. Fading Warsh – EURUSD

It’s the same story in FX. Warsh’s perceived hawkishness has sparked a broad Dollar rally. In the case of EURUSD, spot now sits 2.1 sigma below Qi model fair value – one of the biggest negative FVGs on record.

Model value is moving lower thanks mainly to rate differentials (higher UST yields) but the sell-off in spot has overshot the re-pricing in bond markets.

Again, if you believe the Fed’s reaction function will prioritise price stability over economic growth, you will overrule a quantitative based signal. Wait for PCE today – a strong print will emphasize the hawkish narrative.

But, for anyone anticipating a soft PCE number or if you think the initial hawkish read of Warsh is misplaced, then be aware macro is suggesting US Treasuries & the Dollar have travelled a fair way already.

Related Articles

Identify price dislocations, opportunities, regimes and sensitivities

1. GS HF VIP vs. VIP Short: Crowding Stress

2. Heavy AI Issuance Creates a Contrarian Credit Opportunity

3. ChiNext: the tape and the model have parted ways

Identify price dislocations, opportunities, regimes and sensitivities

1. US Metals & Mining

2. China vs. India

3. NZDCHF

Identify price dislocations, opportunities, regimes and sensitivities

1. XLF: Running Ahead of Macro Support

2. Sterling looks stretched

3. Tech's Quiet Re-Rating

Identify price dislocations, opportunities, regimes and sensitivities

1. Mag7: Impatience Priced In?

2. EURNOK rally losing macro support

3. US Housing rally runs ahead of macro