1. Mag7: Impatience Priced In?

2. EURNOK rally losing macro support

3. US Housing rally runs ahead of macro

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

1. Mag7: Impatience Priced In?

After a 14% drawdown, Mag7’s 12m forward P/E has compressed to the bottom end of

its 10-year range — both outright and relative to the S&P 500.

Positioning has moved just as fast. PB exposure to Mag7 has collapsed in recent weeks,

suggesting investors have cut risk aggressively.

By 25 June, Mag7 was trading at a 2-sigma discount to Qi model value — a level

reached only four times in the past four years. The last instance was mid-March 2025,

during the tariff shock, and it ultimately offered a value opportunity.

The macro backdrop matters. Five-year inflation expectations have fallen close to oneyear

lows, yet Qi model value for Mag7 needs a healthier reflation mix: higher inflation

expectations alongside stronger GDP — in other words, nominal growth and pricing

power.

The burden of proof on AI monetisation is still there. But the scale of the discount in Qi’s

Fair Value Gap suggests the market may have moved from healthy scepticism to

excessive impatience.

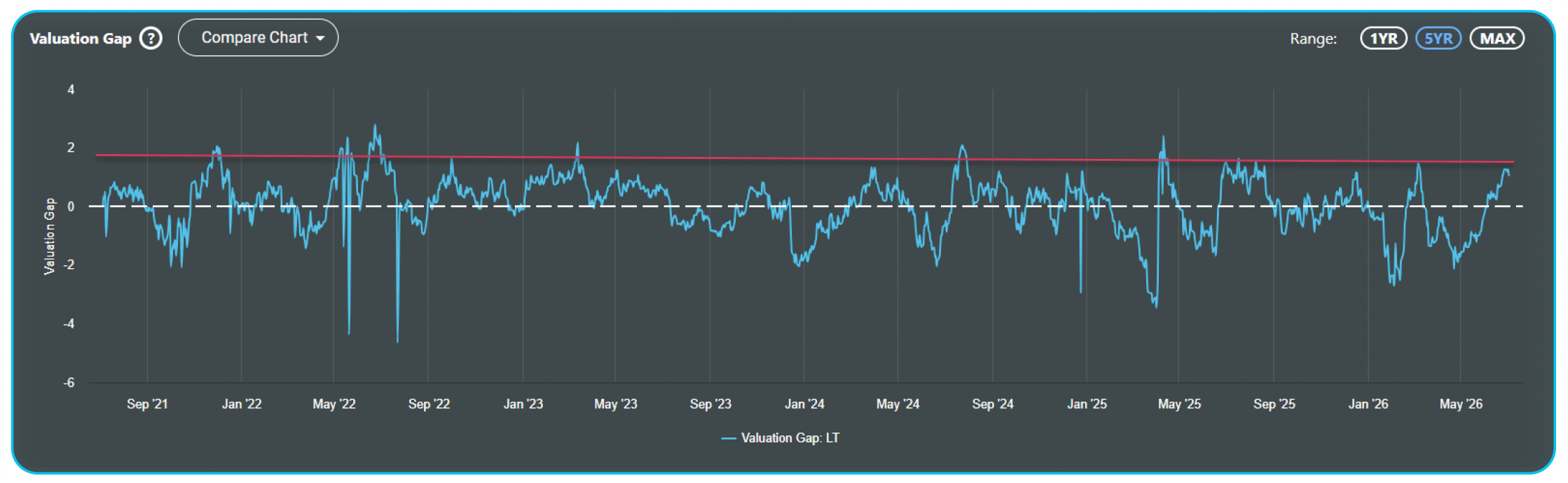

2. EURNOK rally losing macro support

Weaker crude oil plus a perception that the ECB is more hawkish than the Norges Bank

has fuelled a ~5.5% rally in EURNOK since mid-May.

Qi model value over the last month, however, has flat-lined.

Yes, weaker crude has been a tailwind but there have been offsets that mean, on

balance, Qi’s macro-warranted fair value sits around 10.88.

For example, on current patterns the Euro benefits more when metals rally – so the

recent decline in iron ore has been a headwind for EURNOK’s macro environment.

That leaves EURNOK 1.1 sigma rich – very much the top end of FVG ranges.

If you think crude oil has found a floor, that ECB doves are fighting back or the Norges

Bank emphasises inflation running north of 3%, then we have an efficient entry level for

EURNOK downside.

3. US Housing rally runs ahead of macro

The rotation trade has seen housing stocks fare well. Both XHB (Home Builders) and ITB

(Home Construction) have rallied over 20% in the last month.

That’s taken both ETFs to over 1 sigma rich on Qi. Both also show strong (80%)

correlation between Qi’s Fair Value Gap and spot price. When the elastic gets this

stretched, the mean reversion has taken place via the market correcting back to macro

fundamentals.

Qi model value is moving higher but not to the same degree as the market has rallied.

Why?

Some of the good news – both want lower inflation & lower rate volatility – have been

offset by other factors moving the wrong way. Notably higher real yields & a curve

that’s bear flattening when ITX/ XHB want bull steepening.

Macro momentum is rising but the May/June rally has overshot and offers poor riskreward

at these levels.

Related Articles

Identify price dislocations, opportunities, regimes and sensitivities

1. XLF: Running Ahead of Macro Support

2. Sterling looks stretched

3. Tech's Quiet Re-Rating

Identify price dislocations, opportunities, regimes and sensitivities

1. Mag7: Impatience Priced In?

2. EURNOK rally losing macro support

3. US Housing rally runs ahead of macro

Identify price dislocations, opportunities, regimes and sensitivities

1. AI Premium Fades, Macro Discount Still Missing

2. Fading Warsh – 2y Notes

3. Fading Warsh – EURUSD

Identify price dislocations, opportunities, regimes and sensitivities

1. Hang Seng Near Record Cheap vs Macro

2. Falling Inflation, No Value Bid

3. Renaissance IPO ETF - Speculative Risk Is Running Hot