1. Hang Seng Near Record Cheap vs Macro

2. Falling Inflation, No Value Bid

3. Renaissance IPO ETF - Speculative Risk Is Running Hot

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

1.Hang Seng Near Record Cheap vs Macro

The Hang Seng trades -2.44σ (-7.07%) sigma below Qi model value, close to record lows. That underperformance is notable given the recent enthusiasm around Chinese open-source AI models, yet the index is still only up around 1% over the last year.

The valuation gap has opened up over the past month as rate vol has fallen, lifting model value, while the index has failed to follow. That should matter for Hong Kong/China equities, which remain heavily de-rated and highly sensitive to global liquidity. Qi macro explanatory power is high at 74%.

The message is clear: the macro backdrop has improved, but investors still refuse to re-rate China.

The overhangs are familiar: weak domestic demand, property stress, policy credibility, geopolitics, and doubts over whether AI optimism can become an earnings story rather than just a sentiment story.

For now, the market is still pricing China through the lens of risk premium, not growth optionality.

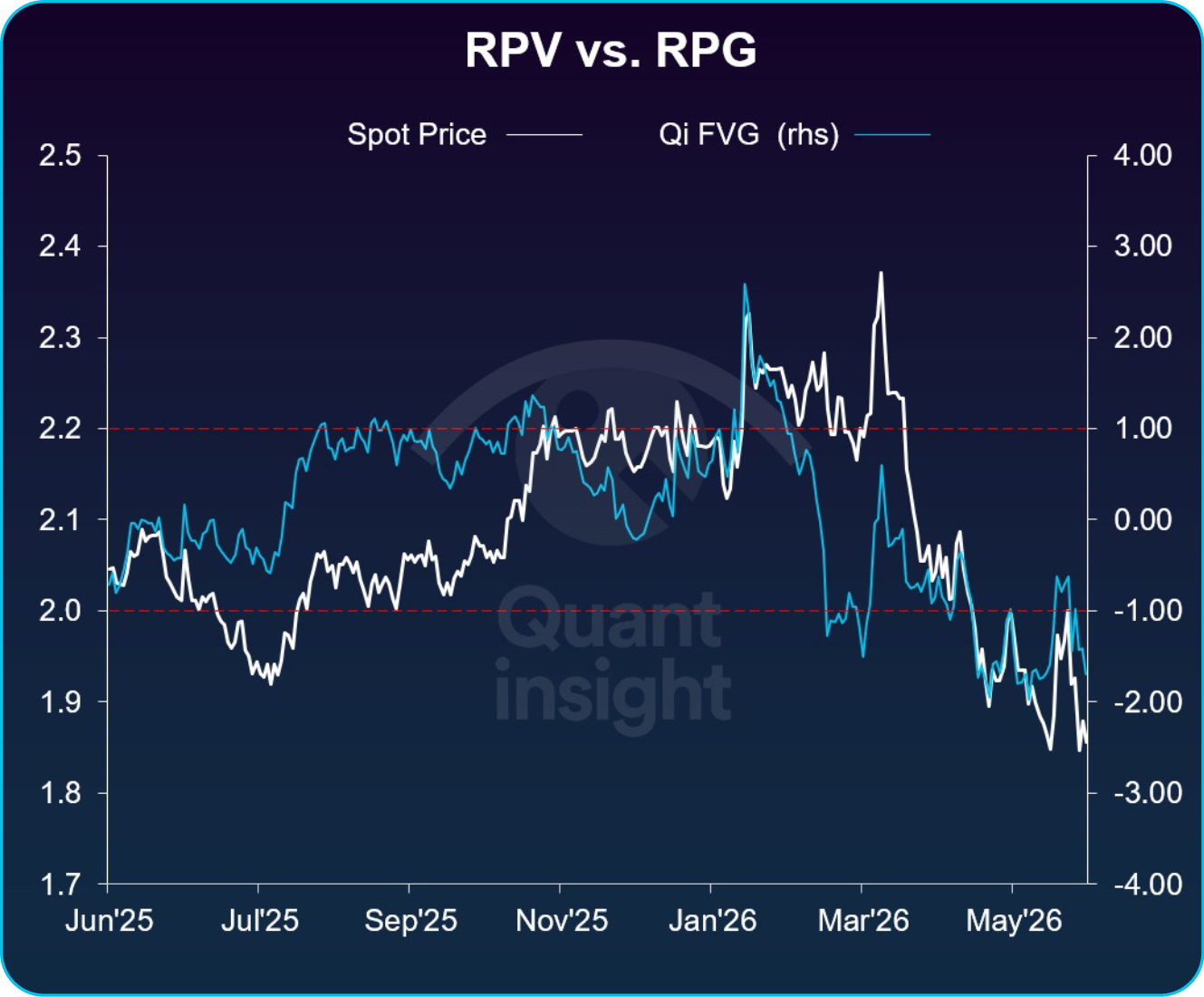

2. Falling Inflation, No Value Bid

The Invesco Pure Value ETF vs. Pure Growth ETF trades 1.7σ (10.57%) below Qi model value - at the lower end of its 5yr range. The relative pair itself is also close to 5-year lows, showing how persistent the Growth leadership has become.

Qi model confidence is high, with macro explanatory power at 72%. The valuation gap has opened because the macro impulse has moved in Value’s favour: 5-year US inflation swaps have fallen, which should reduce pressure on Value relative to Growth.

But price has not followed.

That is the message: the macro backdrop says Value should be doing better, but the market is still paying for Growth dominance.

Either Value catches up as falling inflation expectations broaden market leadership, or Growth continues to defy the macro signal because earnings momentum and AI optionality remain the dominant drivers.

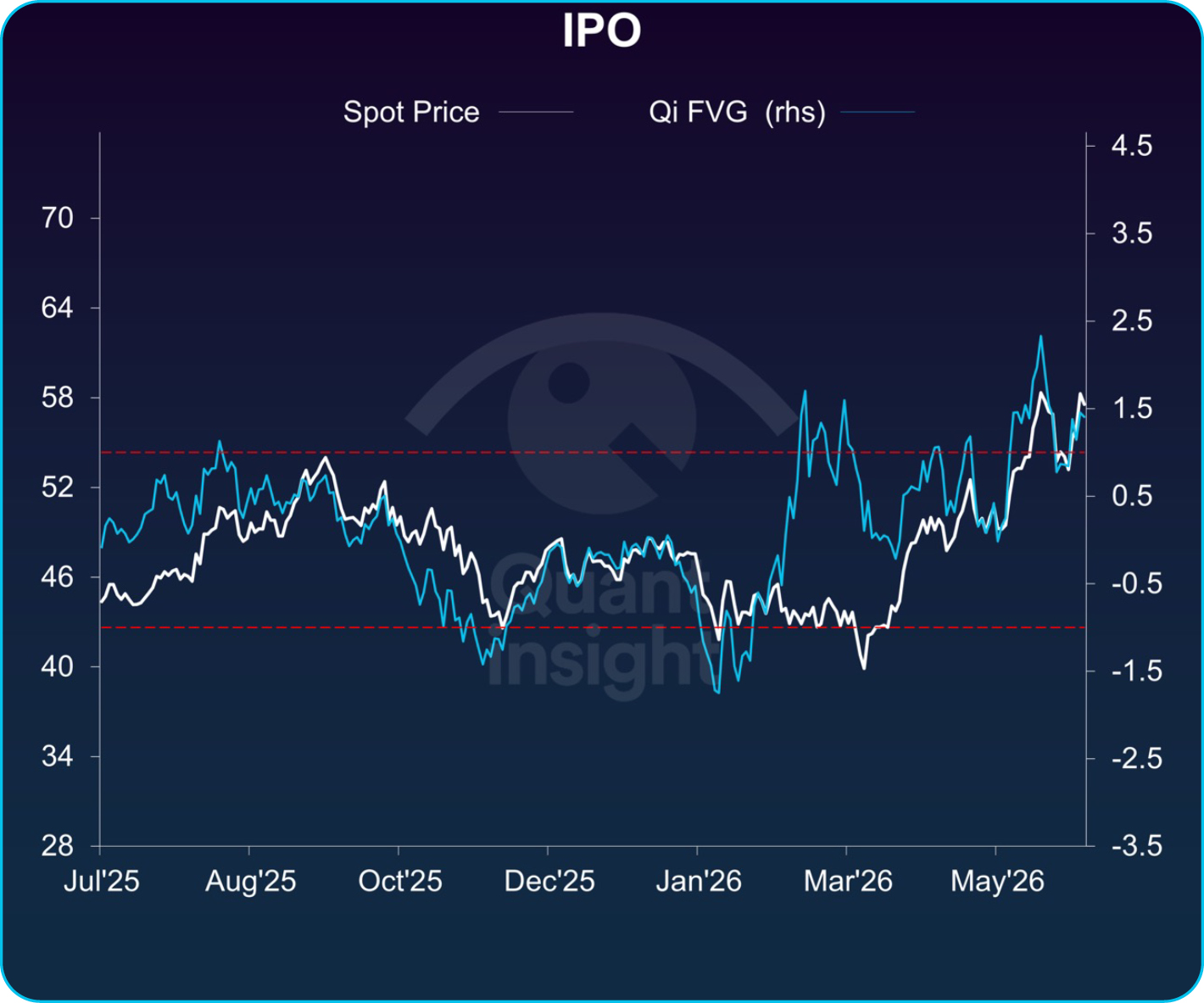

3. Renaissance IPO ETF - Speculative Risk Is Running Hot

The Renaissance IPO ETF sits +1.46σ (9.83%) rich to Qi model value, back at the top of its range after a recent spike toward +2.3σ (13.27%). That matters because this is no defensive basket. It is a high-beta proxy for speculative growth, the part of the market most geared to liquidity, sentiment and future earnings stories. The chart shows the gap repeatedly stretching to these levels and then mean-reverting. This time it has widened as spot pulled away from fair value, so it is no longer just macro-backed risk-on. It is investors paying up for beta.

SpaceX completed the largest listing on record this month, and easing geopolitical risk has revived appetite for newly listed growth. But at +1.46σ rich, a lot of good news is already in the price.

Bottom line: rising beta appetite is the message. IPO US Equity is behaving like a speculative risk barometer, and right now that barometer is running hot. One to watch rather than chase up here.

Related Articles

Identify price dislocations, opportunities, regimes and sensitivities

1. GS HF VIP vs. VIP Short: Crowding Stress

2. Heavy AI Issuance Creates a Contrarian Credit Opportunity

3. ChiNext: the tape and the model have parted ways

Identify price dislocations, opportunities, regimes and sensitivities

1. US Metals & Mining

2. China vs. India

3. NZDCHF

Identify price dislocations, opportunities, regimes and sensitivities

1. XLF: Running Ahead of Macro Support

2. Sterling looks stretched

3. Tech's Quiet Re-Rating

Identify price dislocations, opportunities, regimes and sensitivities

1. Mag7: Impatience Priced In?

2. EURNOK rally losing macro support

3. US Housing rally runs ahead of macro