1. Japan- End of an Era

2. US Industrials- Outperformance due a pause

3. XLP vs. XLY - which consumer bet does macro favour?

4. The Jamie Dimon trade

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

1. Japan - End of an Era

Rates lower-for-longer, QE, Yield Curve Control, carry unwinds, repatriation. Ground Zero for a lot of the major global macro themes live in the Japanese government bond market where 30y yields have hit all-time highs. Whatever the catalyst - a poor auction, fears a US trade deal has to wait until after the summer election - the moves in JGBs are critical for all investors.

The implications will resonate globally but we start by focusing on Japanese stocks. The major drag to the Topix Banks sector today is a steepening of the 5s30s yield curve – the chart below shows the negative sensitivity close to multi-year extremes. If long-end re-pricing fears do not abate, this sector is likely among the most vulnerable.

At the index level, the high negative sensitivity to 10yr JGB real yields is the stand out.In a backdrop where their number 1 export (motor vehicles) face tariff threats,FCIs are starting to matter.

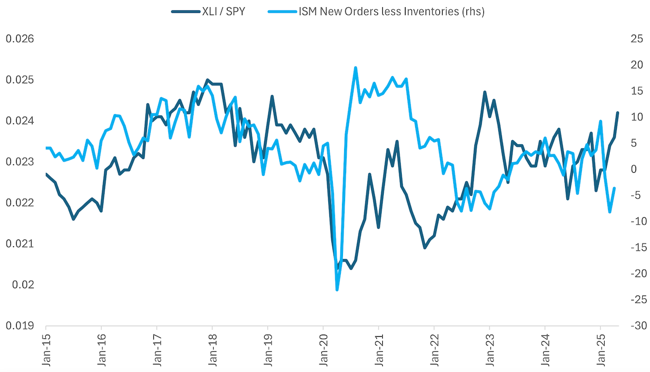

2. US Industrials – Outperformance due a pause

Across the major sectors, S&P500 Industrials isthe only cyclical sector that has made new highs. Recession odds have diminished allowing renewed focus on reshoring, infrastructure and aerospace & defense prospects.

However, we note the sector’s recent outperformance has diverged from the lacklustre ISM new orders less inventories ratio which still sits in negative territory.

Through the lens of Qi, Industrials are the most expensive major sector in the S&P500 – both in absolute terms (+1.5 sigma) and relative to the broader market (+2.5 sigma). Indeed, relative to the broader market, Qi’s FVG is close to multi-year highs.

Since 2009, there have been only 9 occasions where the Qi FVG was > 2 sigma. For 6 of those 9 events, the RV pair lost momentum over the subsequent month. Furthermore, the close relationship between the FVG and spot price, suggests we should be wary of mean-reversion potential.

3. XLP vs. XLY – which consumer bet does macro favour?

Qi's model for the RV between Consumer Staples and Consumer Discretionary is interesting here:

· model confidence is grinding higher

· the regime reveals the safe haven properties you'd expect - XLP outperforms when there's disinflation, credit spreads widen & the Dollar weakens (aka the "sell America" theme).

· XLP screens as 1 standard deviation (~10%) cheap to XLY relative to macro conditions.

Bulls can look away now but, for anyone looking for downside protection, Qi is flagging there's an efficient entry level on this classic defensive bet.

4. The Jamie Dimon trade

Jamie Dimon has warned of complacency in credit markets calling them "a bad risk" and not adequately reflecting recession concerns.

Screening Qi's credit models and the main observation is US/European credit spreads are all marginally too tight. Most FVGs are within 0.5 sigma which means they're too close to macro-warranted model value to get excited. European credit screens as slightly richer than US credit; and EU High Yield spreads sit the furthest through Qi fair value (0.5 sigma, ~14bp rich).

Again, these are not big FVGs in outright terms but strong correlation between spot spreads and Qi FVG suggest our model has done a good job of capturing local tights in XOver. The model does agree with Dimon's basic sentiment - the risk/reward doesn’t look great here.

.png)