1. Higher US inflation winners: China A-Shares

2. Higher US inflation losers: US Real Estate

3. What next for USTs?

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

1. Higher US inflation winners: China A-Shares

China A shares momentum has been gathering pace since June – rallying ~11%.

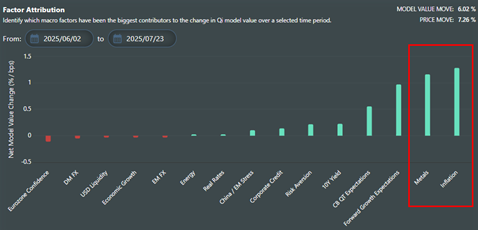

Qi’s valuation model sees rising US inflation expectations as the key driver.

The Michigan survey of long run consumer inflation expectations is currently 3.6%; while the 10yr US breakeven at ~2.6% is as high as we saw last in 2023.

Couple this with concerns on the impact of tariffs and the threat to an independent and credible Fed - we may be losing the anchor to long term inflation expectations.

Qi’s short termmacro model explanatory power for the CSI 300 sits at a high 91% and model price momentum has been rising since June.

The biggest driver of that model price momentum? US inflation expectations followed by industrialmetals.

There is no major valuation gap (CSI 300 is +0.2 sigma rich), i.e. we must pay attention to these drivers. Higher US inflation expectations may encourage diversification away from the US towards cyclical heavy, emerging market exporters.

2. Higher US inflation losers: Realestate

At the other end of the spectrum are a bunch of US real estate plays. ITB (Home Construction), XHB (Homebuilders), IYR (Real Estate) all screen as close to 1.5 sigma rich on Qi. And all three have negative sensitivity to inflation expectations as their biggest macro driver.

Chart patterns look attractive with leading stocks like DR Horton breaking out. But while technical analysts are typically turning constructive, macro offers a warning – current patterns show the sector is particularly vulnerable to an inflation scare.

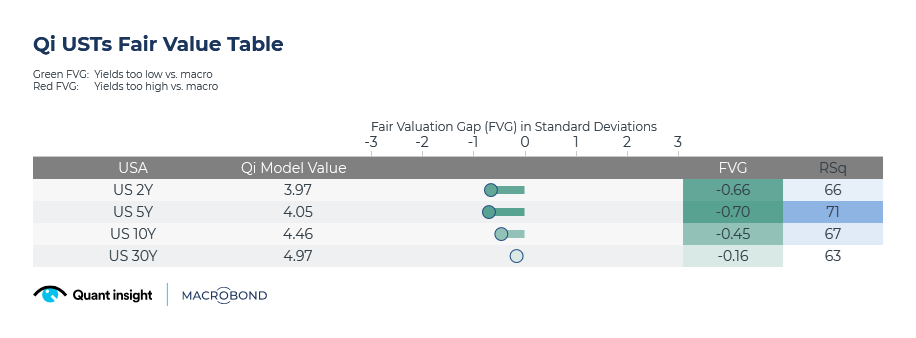

3. What next for USTs?

US Treasury yields have not kept pace with rising inflation expectations which are the biggest macro driver on Qi's models.

That leaves US bond yields as too low versus prevailing macro conditions.

The Valuation Gaps are smaller but, for deficit hawks, 10y & 30y yields probably offer the more intuitive opportunity.

In pure Qi FVG terms, 2y & 5y look better entry levels for bond bears. That will suit those whonote the debate around a change in Fed leadership has seen the market re-price the terminal rate to the bottom of the range (~3%) that's held since the 2022 tightening cycle. But no further.

In other words, thus far the market expects a new Fed Chair speeds up rate cuts but doesn’t necessarily cut more. In which case the risk-reward for the front end is starting to look stretched with 2&5y yields down here.

.png)