1. Stocks discounting further tightening in US HY Credit?

2. EFA - The easy vol reset has ben done

3. USD-Asia On the move I

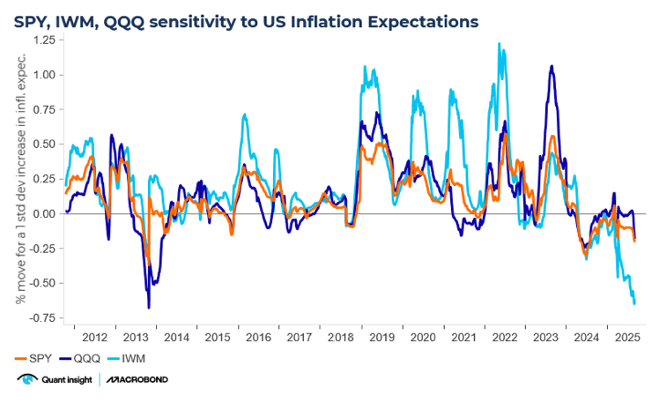

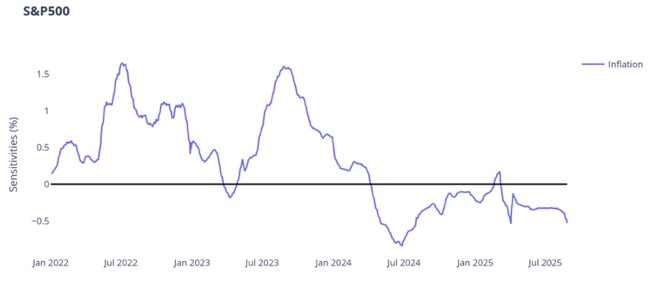

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

1. Stocks already discounting further tightening in US HY credit?

Qioffers macro tracking equity baskets (tradeable with Goldman Sachs). We usemachine learning to identify a selection of stocks and their weights, which arethen traded out of sample for a month and then re-balanced to keep adapting tomarket conditions. We offer a long / short pair to track HY credit spreads(GSQIHYLL (long leg) / GSQIHYLS (short leg).

Thefirst chart below shows the Qi credit tracker pair vs. HY credit spreads. Theformer appears to discounting ~360bps HY spreads vs. spot of 391bps.

Similarly,the second chart show only the short leg vs. the inverse of HY credit spreads(i.e. you profit from shorting the basket when HY spreads widen). This is alsodiscounting ~350bps HY spreads.

Theconclusion is that the easy reset in vol has been done. Despite the hopium onChina / US talks next week, a lot is already priced. Even if China tariffs arereduced to 60%, it will still hurt the growth / inflation tradeoff.

Ifat 6000 SPX zero recession odds are priced and at 4500, a 25% decline, 100%recession odds then today ~20% recession odds are priced. It gets harder fromhere – that China does not give in easily is a distinct possibility.

2. EFA – the easy vol reset has been done

The Dollar denominated EFA ETF (MSCI EAFEindex which represents DM in RoW) is today at new all-time highs. Last week, wesaid Japanese equities in Dollar terms was looking over-extended. Qi shows EFAat +1.65 sigma above its macro-warranted fair value. This level of Fair Value Gapis close to record highs. Whilst spot has made new highs, the Qi model valuefor this ETF has not.

Markets have come a long way given depressedpositioning alongside the view that incremental tariff news will be positive.There will also be hope next week of a deal between the US & China.However, even tariffs on China back at 60% (which is where expectations wereduring Trump’s presidential campaign) and 10% elsewhere will hurt. We may endup with a dose of “travel & arrive”. Meanwhile, European earnings seasonhas failed to drive earnings expectations higher – it has been all about PEexpansion (no longer cheap vs. history), not earnings delivery.

3. USD-Asia on the move I

Asia accounts formore than half the US's trade deficit. That fact alone supports the ideaDollar-Asia is entering a new multi-year re-pricing. There were already manybelievers in the idea of lower USDJPY, but does the two-day 10% move in USDTWDor the HKMA announcement about diversifying into non-US assets add fuel to thefire?

Positioningand macro suggest these are not the best levels to chase USDJPY downside. Firstconsider the latest Commitments of Traders data – speculators are running thebiggest net Yen long in history.

Second,USDJPY sits 1.3 sigma (4.2%) below Qi’s macro-warranted model value.Aggregating across rate differentials, shifts in respective 5s30s yield curves,spikes & subsequent retracements in VIX & credit spreads, model valueis flat-lining. Macro conditions have not vindicated the latest downtick,instead suggesting the cross should trade near 150.

Disclaimer

This document is being sent only to investment professionals (as that term is defined in article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) OrdeRSq005 (“FPO”)) or to persons to whom it would otherwise be lawful to distribute it. Accordingly, persons who do not have professional experience in matters relating to investments should not rely on this document. The information contained herein is for general guidance and information only and is subject to amendment or correction. This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This document is provided for information purposes only, is intended for your use only, and does not constitute an invitation or offer to subscribe for or purchase any securities, any product or any service and neither this document nor anything contained herein shall form the basis of any contract or commitment whatsoever. This document does not constitute any recommendation regarding any securities, futures, derivatives or other investment products. The information contained herein is provided for informational and discussion purposes only and is not and, may not be relied on in any manner as accounting, legal, tax, investment, regulatory or other advice.

Information and opinions presented in this document have been obtained or derived from sources believed to be reliable, but Quant Insight Limited (Qi) makes no representation as to their accuracy or completeness or reliability and expressly disclaims any liability, including incidental or consequential damages arising from errors in this publication. No reliance may be placed for any purpose on the information and opinions contained in this document. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Qi, its employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions. Any data provided in this document indicating past performance is not a reliable indicator of future returns/performance. Nothing contained herein shall be relied upon as a promise or representation whether as to past or future performance.

This presentation is strictly confidential and may not be reproduced or redistributed in whole or in part nor may its contents be disclosed to any other person under any circumstances without the express permission of Quant Insight Limited.

.png)